")

")

| Issue |

Matériaux & Techniques

Volume 111, Number 4, 2023

Special Issue on ‘The role of Hydrogen in the transition to a sustainable steelmaking process’; edited by Ismael Matino and Valentina Colla

|

|

|---|---|---|

| Article Number | 405 | |

| Number of page(s) | 9 | |

| Section | Metals and alloys | |

| DOI | https://doi.org/10.1051/mattech/2023030 | |

| Published online | 14 December 2023 | |

Original Article

Pathways towards full use of hydrogen as reductant and fuel

Linde GmbH, Carl-von-Linde-Strasse 25, 85716 Unterschleissheim, Germany

* e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Received:

1

June

2023

Accepted:

3

November

2023

Abstract

The transition to a green steel making is a journey over decades that involves many technologies and pathways, in most scenarios with the use of hydrogen − both as reductant and as fuel − as the endgame. The paper describes a general pathway to decarbonisation including increased energy efficiency, use of low carbon fuels, carbon capture, and use of clean hydrogen as reductant and fuel. The possibilities for developing a greener blast furnace process as a short-term solution, is discussed. Combinations like direct reduced iron production with carbon capture using a gasified waste or biomass, could be a mid-term solution at some steel mills. Dependent on location-specific conditions some technologies, like use of hydrogen as fuel in reheating, is coming into use already now, whilst in other areas in near- and mid-term there will be intermediate solutions applied. Development of hydrogen production technologies is briefly described. Challenges for the transition are found not only within the steel industry itself, but also, e.g., in supply of renewable power and suitable iron ores. Moreover, potential supply chain integrations and impact of geographical dislocations are discussed. Overall, it is important to apply an integrated approach with clear milestones for the chosen pathway, where existing assets like blast furnaces are transformed into a lower carbon footprint operation applying technologies that also can be used in the subsequent transition, e.g., use of coke oven gas for producing direct reduced iron that is charged into blast furnaces where carbon capture is applied, or changing into more energy-efficient combustion systems that are ready for use of hydrogen when viably available.

Key words: Steel / decarbonisation / hydrogen / energy-efficiency / carbon footprint

© J. von Schéele, 2023

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

1 Introduction

The steel industry ranks amongst the top three CO2 emitters from the industrial segment. Consequently, the pressure to decarbonise steelmaking has led many producers to set carbon neutral goals over the 2030–2050 timeframe. But how are those goals to be achieved? Based on the individual preconditions, it is important to develop and deploy roadmaps that include both near term actions and, in parallel, longer-term activities broken down as measurable milestones. The transition of the industry, which is the aggregated result of the actions of each individual plant, is a journey that will span decades.

In 2022 the world steel production reached close to 1,880 million tonnes (Mt), with a supply of iron for that steelmaking being around 1,300 Mt of hot metal from blast furnaces and more than 90 Mt of Direct Reduced Iron (DRI) produced using natural gas as reductant; the amount of DRI produced using coal as reductant was about 30 Mt [1–3]. Additionally, 770 Mt of scrap were charged. Steel is the most recycled material in the world, and the first step to achieve sustainability and decarbonisation is to maximise the degree of recycling. Between the years 2000 and 2010, the world steel production grew by more than 700 Mt/a; predominantly in China, where today more than half of the world steel production takes place. This is resulting in a massive increase in availability of scrap for years to come. Clearly, this will have a very positive impact on the carbon footprint of the steel industry, as the increase in scrap supply will be larger than the growth of steep production. However, for the next decades most of the raw material for steel production will remain hot metal.

While electrification is the direct route to decarbonise many processes, many unit processes in steel production are extremely difficult to electrify − these include processes for iron ore reduction, as well as heating processes which use large scale high temperature combustion in a steel mill. For such processes, the main options include use of oxyfuel combustion to achieve increased energy efficiency, introduction of low carbon fuels, and carbon capture. Ultimately, the use of clean hydrogen as a reductant as well as a fuel source is the endgame that steelmakers will adopt when a viable supply of hydrogen becomes available [4,5]. Accordingly, there is a general pathway to decarbonisation [6]:

Increase energy efficiency, e.g., by using oxyfuel combustion

Use of low carbon fuels

Carbon capture

Use of clean hydrogen as reductant and fuel

Over the next decades a large transition will take place, but it will take time and involve multiple solutions − some more of incremental in their nature, some more disruptive − and the pace will be different in different parts of the world. The drive from the market to produce steel with a low carbon footprint and availability of a viable supply of clean energy are two important factors.

The paper discusses how the dominant production route can be decarbonised by making “a greener blast furnace”, possibilities and challenges when increasing the production and use of DRI − particularly using hydrogen −, how increased energy-efficiency in combustion processes immediately supports decarbonisation and prepares for use of hydrogen as fuel, scale-up and cost of hydrogen supply, and ends with a discussion on the impact on the steel production value-chain and the industry structure. Figure 1 is an attempt to summarise the expected general development over the coming decades, which is discussed in this paper. Certainly, the pace will be different in different parts of the world, and viable supply of renewable power might be more pace-determining than technology.

|

Fig. 1 The transition into low-carbon footprint steelmaking with near-term activities, multiple solutions, and long-term development projects. |

2 A greener blast furnace

Integrated steel mills, which produce steel from iron ore, account for 70% of global steel production but emit almost 90% of CO2 emissions due to their high CO2 intensity of 2.3 tonne of CO2 per tonne of steel produced (Scope 1–3). In contrast, so-called mini-mills using the Electric Arc Furnace (EAF) process with recycled steel scrap as primary feedstock, account for the balance 30% of global steel production but only 10% of emissions since they emit 0.6 tonne of CO2 per tonne of steel produced [1].

While mini-mills have the potential to eliminate almost all their CO2 emissions by using renewable electric power and green hydrogen in their existing production plants, integrated mills cannot − the blast furnace in an integrated mill requires a certain minimum level of coke (practically around 300 kg/t) to operate with attendant CO2 emissions from its use. Therefore, integrated mills either need ways to capture and sequester all their CO2 emissions, or they require a fundamental change to the processing route away from the blast furnace, with concomitant CAPEX and OPEX implications.

Accordingly, from a global perspective the prime focus to achieve decarbonisation should be on the ironmaking step as this is where the majority of the CO2 emissions are generated. If the blast furnace smelting route is replaced by direct reduction producing sponge iron (DRI), the mentioned carbon footprint would drop from 2.3 to 1.6 even when using natural gas as reductant. DRI production will be discussed later in this paper.

An integrated steel mill has multiple points of CO2 emissions: in the blast furnace gas, stoves, coke ovens, sintering/pelletizing lines, etc. Most carbon capture efforts have focussed on capturing the CO2 from blast furnace gas (BFG), which is mostly emitted in the flue gas of the power plant where the BFG is used. The other sources of CO2 emissions are generally not considered for economic reasons, but they need to be evaluated as part of an overall Carbon Capture Use and Sequestration (CCUS) optimisation approach as CCUS technologies become more economical.

Another concept being considered to decarbonise blast furnaces is to recycle the BFG after separation and removal of CO2 (and potentially nitrogen). The balance of BFG contains CO and H2 that can be recycled and used as a reductant in the blast furnace. This requires significant additional CAPEX investment, and it is therefore only applicable for blast furnaces which are expected to have a long lifetime to assure the return of investment on this capital. This also impacts the overall gas balance in the steel plant and it eliminates the use of BFG for power generation, which may be a desired outcome due to its high carbon footprint.

Use of oxyfuel combustion supports viable use of BFG and other low-caloric gases for heating purposes, e.g., at ladle preheating and in reheat furnaces. Use of BFG in such downstream processes could replace externally supplied natural gas.

Moreover, there are interesting options for chemical valorisation of BFG, for example by synthesising into by-products like methane and methanol [7–10]. The steel mill could be seen in a larger context, guided by symbiosis structures involving additional value-streams and providing an overall positive result on decarbonisation. In this context could also be mentioned the interesting work by companies using microbes, such as LanzaTech, for which now production of bio-ethanol has begun in the Steelanol project at a steeelworks in Belgium [11,12].

Blast furnaces use oxygen enrichment of the cold blast to improve productivity and to enable the use of injectants through the tuyeres that reduces CO2 emissions. Many blast furnaces operate with up to 30% oxygen in the blast today. In addition to the cold blast, oxygen can also be used in blast furnace stoves, which is a short-term way to increase the energy efficiency. Stove Oxygen Enrichment (SOE) is a method to add high-purity oxygen to the stove combustion air to eliminate the use of sweetening high-value fuels like natural gas or coke oven gas, raise blast temperature and de-bottleneck plugged stoves. Evaluations show that a 100 °C increase in blast temperature translates into coke savings of 8–12 kg/t of hot metal, with attendant reduction in CO2 emissions, which has also been confirmed in theoretical studies [13]. SOE has been successfully implemented in at least 14 blast furnaces in the Americas, Asia, and Europe [14].

The conversion of the blast furnace stoves to full oxyfuel combustion, along with attendant recycling of the flue gas to control temperature, allows the CO2 emissions to be concentrated and minimise CO2 capture costs. This approach is recommended to optimise multi-point CO2 capture in a steel mill.

In the short term, charging of scrap and not at least DRI into the blast furnace could be good ways to the decrease its CO2 emissions. While DRI is mostly charged into EAFs, it can also be briquetted into Hot Briquetted Iron (HBI) and charged into blast furnaces or steelmaking converters to achieve decarbonisation in an integrated steel mill. As a rule-of-thumb, each 10% increase in burden metallisation in a blast furnace by the addition of HBI increases the production rate by 8% and decreases the coke rate by 7%, with attendant CO2 savings [14].

While hydrogen is generally considered as the ultimate low or zero carbon fuel of the future, there are other approaches to low-carbon fuels in the near term with feedstocks derived from biomass, waste plastics, Municipal Solid Waste (MSW), etc. The coke rate in blast furnaces can be lowered using injectants through the tuyeres with a lower carbon footprint, such as pulverised coal, natural gas, coke oven gas, and potentially hydrogen in the future. For example, every ton of injected coal avoids 0.85–0.95 tonne of coke production, with accompanying energy savings of around 3.75 GJ/t injected coal. However, tuyere injection has its limits due to a negative impact on the Raceway Adiabatic Flame Temperature and the ability to combust certain injectants within the confines of a tuyere. These limits can be raised if the injectants are first gasified into a syngas (CO + H2) externally, prior to injection into the tuyeres. This external gasification can be performed by, for example, the Hot Oxygen Technology (HOT) − a fuel flexible tool to gasify solid, liquid, or gaseous feedstocks including natural gas, coke oven gas, wide varieties of biomass, waste plastics, MSW, etc. A typical HOT system is an efficient, small-scale gasifier to generate reducing gas or syngas up to 35,000 Nm3/h per unit. Multiple units can be employed to meet the requirements of a blast furnace. This approach helps to minimise the CO2 footprint of an existing blast furnace without significant modifications to the production process [15].

The use of hydrogen injection into blast furnaces has been tested on a minor scale. To a certain extent hydrogen injection is beneficial, however, vast hydrogen volumes would be required. A limited use of hydrogen injection could take place at certain locations with favourable cost conditions, but it does not seem this will play a major role in the transition to a reduced carbon footprint.

3 DRI and EAF

The Swedish Professor Martin Wiberg (1894–1975) was the father of shaft-based Direct Reduction processes, later to be developed into well-known processes such as Midrex (1969), HyL (1957/1980), etc. Wiberg and coworkers started pilot scale tests at Voxna Bruk in 1920. Later followed full-scale operations at many other Swedish locations: Söderfors (1933–1961) at 10 kt/a; Sandviken (1952–1980) at 20 kt/a; Hällefors (1953–1963) at 20 kt/a; Persberg (1953–1973) at 40 kt/a; and Hofors (1955–1978) at 30 kt/a [16].

DRI is today predominantly produced with natural gas as the reducing gas in shaft furnaces. As mentioned above this production has already reached 90 Mt/a, i.e., coming a long way beyond what took place in Sweden in the mid of the previous century. DRI or, more likely, HBI can be used as a feedstock in blast furnaces, providing both a lower carbon footprint there and an increase throughput rate. Naturally, this is particularly of interest if the HBI itself carries a low carbon footprint, produced using − partly or fully − clean hydrogen or natural gas with CCUS. However, the focus beyond a transition period is use of DRI/HBI in electric furnaces, EAFs or electric smelting furnaces.

It should be noted the earlier mentioned HOT system can also be used to deliver reducing gas or syngas to a DRI plant, derived from a variety of sources including coke oven gas, and replacing the need for natural gas. Extensive work has taken place at the DRI plant maker MIDREX to develop the Thermal Reactor System (TRS) that will produce clean syngas from coke oven gas and other hydrocarbon sources for DRI production [15]. TRS utilises partial oxidation technology, using HOT, which offers the potential to do partial oxidation of hydrocarbons without steam injection. When this technology is combined with an extended reaction chamber into which a preheated stream of coke oven gas is added, the product gas leaving the chamber is suitable for direct use as a reducing gas to produce DRI. Figure 2 shows how HOT can be used to supply both blast furnace and DRI operations.

Accordingly, there is an option to produce a low carbon footprint syngas to be used both in blast furnaces and direct reduction shafts that is based on waste plastics, MSW, biomass, etc. Thereby we can not only reduce the steel industry’s carbon footprint but also contribute to solve a waste problem and support a circular economy, but also create a carbon sink. In general, the use of biomass as a reducing agent is of interest as it can create even a “carbon sink”, i.e., providing a resulting carbon footprint that is below zero [17].

The DRI-EAF route is the most commercially ready path to full decarbonisation for integrated steel mills. Over 90 Mt/a of DRI is produced today in shaft furnaces with natural gas as the reductant. Considering Scope 1–3, an integrated mill can decrease its CO2 footprint from 2.3 to below 1.6 t/t of finished product by switching to this processing route, potentially at the time of blast furnace relines to minimise incremental investments. Thereafter, CO2 emissions can be dropped further down to almost zero by using green hydrogen as the reductant instead of natural gas, along with green power to the EAF and balance of plant. While up to 70% hydrogen has already been demonstrated in a DRI plant, pushing this limit to 100% hydrogen is the focus of several pilot plants that recently have been initiated. An important difference between use of natural gas and pure hydrogen, however, is the endothermic nature of reduction with hydrogen, which requires a preheating of the hydrogen to temperatures around 900°C (and not needed when using natural gas as reductant). Additionally, a large obstacle for expanding the production of DRI is availability of suitable iron ore pellets.

It is obvious from the above considerations that near complete decarbonisation is possible, but at severe costs which need to be offset with higher costs of CO2 emission. This decarbonisation also requires significant investments in new facilities and assets − a daunting challenge for this industry to overcome. For example, the CAPEX for a H2-DRI-EAF plant could be 800–1,000 $/t of annual capacity, but after factoring the cost of the required green power and hydrogen infrastructure, these costs can escalate to 5,000 $/t of annual capacity. Clearly, this is a long-term solution for the industry, beyond year 2030 for most locations around the world [18].

|

Fig. 2 The hot oxygen technology can support a circular economy using gasification to produce low-carbon footprint syngas for ironmaking processes. |

4 Combustion operations

Though the reduction processes are very much in focus due to being the main contributor to the carbon footprint of iron and steel making, attention should also be paid to the combustion processes. Naturally, the relative importance of those processes in this context is larger at minimills than at integrated mills, not to mentioned at re-rollers. Downstream steel processing − including rolling, heat treatment, and finishing − accounts for a significant portion of direct specific CO2 emissions. In case of the scrap-based minimills that figure is around 50%.

Oxyfuel combustion technology is a solution for immediate decarbonisation, which also allow smooth adaptation to hydrogen fuels whenever viable. Many unit operations in a steel mill use air for the combustion of fuel, which carries 79% ballast (almost all of it nitrogen). This nitrogen is heated up in the furnace and emitted in the flue-gas, resulting in wasted energy, higher fuel consumption and CO2 emissions. Moreover, it hampers the radiative heat transfer from the products of combustion, which is the dominant mechanism at elevated temperatures. The use of oxygen instead of air, called oxyfuel combustion, eliminates this nitrogen ballast, and results in:

up to 60% fuel and CO2 savings,

75% reduction in flue-gas volume,

up to 90% NOx reduction,

on-demand production increase, and

ability to use of low calorific gases in heating and reheating operations.

The economics of oxyfuel combustion are typically driven by fuel price, but as steel mills adopt green hydrogen fuel to decarbonise their footprint, oxyfuel combustion will become economically necessary. This is because hydrogen prices are expected to drop down to around 2$/kg, which is equivalent to 15$/GJ, i.e., hydrogen will always be a relatively expensive fuel; accordingly, oxyfuel combustion is required to minimise its use. Therefore, the recommendation to steel mills is to convert to oxyfuel combustion now to achieve 20–50% CO2 reduction and be prepared to increasingly blend in green H2 as and when it becomes available to achieve full decarbonisation in the future.

Given high fuel prices and the need to decarbonise, oxyfuel combustion offers an immediate first step for steel mills to adopt across their flow sheet. Oxyfuel combustion has been successfully applied to several steel mill operations including blast furnace stoves, pelletizing/sintering furnaces, electric arc furnaces, ladle preheating (40–60% fuel savings), reheat furnaces (batch and continuous) and heat treatment furnaces. Oxyfuel combustion, producing a much smaller flue-gas volume with a high concentration of CO2, also supports CCUS. Use of stove oxygen enrichment is a well proven options that can be comparatively easily deployed at integrated steel mills saving high calorific fuel and CO2 emissions. In melting, preheating, and reheating, proven oxyfuel technologies are available to successfully create decarbonisation, using hydrogen now or later. Oxyfuel solutions can be applied immediately, and at many steel mills with very short payback periods.

Numerous tests have been made over the past five years using hydrogen as a fuel in combination with oxyfuel combustion [19–21]. It has been concluded that those proven and well-established solutions, both for conventional oxyfuel and flameless oxyfuel, work very well with hydrogen as a fuel. This has been confirmed in full-scale tests in operation. For example, to decarbonise the chemical energy input into EAFs, CoJet injectors have been developed into use of hydrogen as fuel with excellent results. Hydrogen extends the coherent jet length, increases heat transfer, and reduces maintenance of the injectors. These features make hydrogen an ideal fuel for the CoJet system − also from an operational point of view − and pave the way to fully decarbonise the EAF [22,23] Figure 3 shows an image of the CoJet flame shrouding.

Looking at reheat furnaces, several full-scale tests have been carried in production, and now those flameless oxyfuel technologies are all hydrogen-ready [24–26]. The first permanent installations using 100% hydrogen as fuel in 24 soaking pit furnaces, are being commissioned at Ovako Steel in Sweden in Q4 of 2023. Figure 4 shows an image from the full-scale test there in March 2020. In this test 25 tonnes (six 4.2 t ingots) of ball bearing steel were successfully heated, processed downstream, and sold to customers.

Moreover, use of flameless oxyfuel in ladle preheating has been proven a great success over the past decades with hundreds of installations delivering massive fuel savings, faster heating, and reduced NOX emissions [27]. Use of hydrogen as fuel in this application has been tested showing encouraging results, and several steel mills are considering deploying it as soon as a viable supply of hydrogen is available at their sites.

|

Fig. 3 CoJet flame shrouding with an oxyfuel flame around the oxygen jet. |

|

Fig. 4 Flameless oxyfuel using 100% hydrogen as fuel at world’s first full-scale test of steel reheating with all hydrogen combustion in March 2020 at Ovako Steel in Sweden. |

5 Scale and Cost of Green Power Supply

To enable the last step of this transition to H2-DRI for full decarbonisation, DRI based steel production will require very large-scale green hydrogen and green power. Considering 63 kg/t of green hydrogen required per tonne of DRI and 12 kg/t for other heating applications in the plant, a 2 Mt/a DRI-EAF plant will require about 1.1 GW of green power to produce the required green H2. For reference, the largest PEM electrolyzer in operation today is 24 MW. Hydrogen suppliers are preparing for this scale up and supply, but the progress is expected to take time. Making an order of magnitude estimate, to convert all 95 Mt/a of blast furnace-based ironmaking in Europe to DRI based, about 17,000 t/d of green hydrogen would be required. Accounting for the power required for the hydrogen electrolyzer, as well as the power for the EAF and other plant operations, the green power requirement for integrated steel production would be about 400 TWh/y. Adding the power requirement for 65 Mt/a of current EAF steel production, the EU28 green power requirement for steel totals 470 TWh/a (54 GW), or around 17% of Europe’s current power consumption. The pace of increasing supply of renewable power to produce hydrogen and to be used in EAFs and electrical smelting furnaces, seems to be a factor that could be limiting the speed of transition [18].

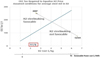

In addition to large scale hydrogen supply, the economics of this transition will require green hydrogen prices to drop significantly below current levels. Naturally, the higher the cost of CO2 emissions (taxes, allowances, etc.), the higher the price that makes the economics of this transition to H2-DRI favourable. Indeed, a combination of increasing cost of CO2 emissions and drop in H2 pricing will be necessary to achieve economical decarbonisation. This is illustrated in Figure 5. Steelmakers are also increasingly focussing on deriving premiums for green steel to justify their investments.

For green hydrogen from electrolysis, the cost is predominantly dependent on the cost of renewable energy. With a stable low-cost supply of renewable energy, a viable supply of hydrogen can be put in place using electrolyzer technology. We can then conceive a plant producing green steel, including hydrogen based DRI production, EAF steelmaking supplied with renewable power, and all combustion process using energy efficient oxyfuel with hydrogen as a fuel. As the electrolyzer produces both hydrogen and oxygen, we would then have a complete integrated system. However, such a plant can also serve in a hub where additional production of hydrogen and oxygen are supplied to neighbouring offtakers. Figure 6 outlines how such an ecosystem could be conceived.

|

Fig. 5 CO2 emission cost versus cost of hydrogen (and electricity) providing areas where hydrogen-based steel is favourable and not. |

|

Fig. 6 Outline of integrated green steel production ecosystem for a 2 Mt/a DRI-EAF steel plant with 100% green hydrogen and oxygen. |

6 Challenges and dislocations

A number of challenges have already been discussed:

Availability of DR grade pellets

Cost of clean power, required for both hydrogen production and electric furnace operation

Large CAPEX requirements

Additionally, there is frequently a mismatch in size and pace of the new operations if they are to be part of an existing integrated steel mill; the tap size weight is smaller and the tap-to-tap-time longer than the existing Basic Oxygen Furnace (BOF) converters. If Blast Furnace grade pellets are used in the DR process, a subsequent electric smelting operation would be required as the conventional EAF cannot handle such slag volumes. In that case the resulting liquid product would be similar to the existing hot metal and it would charge into the BOFs and thereby, potentially, resolving the pacing issue providing enough numbers of electric smelters are employed.

There is a tendency of a forward integration trend in DRI production. Mining companies with suitable iron ore have been supplying DRI based steel plants with pellet feed for making DR pellets or already made DR pellets. We now see mining companies at locations with access to clean energy evaluating projects for forward integration to ship HBI instead of DR pellets or DR pellet feed. Accordingly, such a development entails putting up DRI production facilities, operated either with hydrogen as a reductant or with natural gas combined with carbon capture. An example of such a development is found at LKAB in Sweden whilst other mining companies are exploring possibilities, e.g., in Australia, Brazil, and Canada [28].

When HBI production is established at locations favourable for viable production of clean hydrogen, for example, countries in Africa, it is not far-fetched to envisage a scenario where there is also a flow of hot DRI into a new adjacent EAF mill. And we could then consider potentially two parallel flows of steel products: one catering to an increasing domestic market (probably replacing imports); one exporting semi-finished green steel. Accordingly, we might welcome countries like, say, Namibia into to the fraternity of steel producing countries, but might also see how such green steel will be imported into, for example, Europe replacing some European steel production.

The impact of decarbonisation on the steel industry’s structure and locations is a process and a potential trend, which is likely to be experienced in different ways and at different paces across the world, governed by individual preconditions and local ability to cope with new demands. Backward and forward integration of raw materials supply will be pronounced. Moreover, we are entering an era with significantly increased importance of clean energy supply and operation for the location of ironmaking, which will impact the steel industry structure globally. This dislocation will create winners and losers and have substantial positive and negative local economic impacts.

7 Hydrogen production

For hydrogen supply to iron and steel making operations, large volumes are required. The vast majority of the world’s current hydrogen production is captive and carries a large carbon footprint. For supplying hydrogen to the steel industry new investments are needed in production supplying hydrogen with a low carbon footprint. Hydrogen production with natural gas as feedstock could be combined with CCUS, what many currently refer to as ‘blue hydrogen’. However, the focus has been on ‘green hydrogen’, i.e., hydrogen produced from electrolysis of water using renewable power. There are three main types of electrolyzers: Alkaline; PEM (to be read as Proton Exchange Membrane or Polymer Electrolyte Membrane); and Solid Oxide. Alkaline electrolyzers have been used for many decades and operate at rather large scale, up to hundreds of MW. PEM is a comparatively new technology, where the world’s largest units currently in operation are at around 25 MW, while Solid Oxide is the newest technology, so far only in small scale operation. Given its operation flexibility, PEM is often seen as a main solution in combination with renewable power.

It is expected the costs of electrolysers will drop in the years to come. However, it should be noted around half of the equipment involved comprises well-established ‘standard’ components and processes. Moreover, electrolysers use expensive metals. For example, the electrolysis process needs catalysts to work − and the best current industrial electrodes use precious metals including iridium, ruthenium, and platinum. A third point here is that electrolysers are built in modules, i.e., the impact of scale on the specific investment cost is rather limited; larger electrolysers mean more modules. Accordingly, at this point in time it is advised to be careful with estimations on radically decreased costs of electrolysers in the next years.

Clearly technical developments will increase efficiencies of electrolyzers, bringing the electricity consumption closer to the theoretical limits. This is further supported by use of pressure and temperature. However, even when reduced, the cost of electricity would be the main cost component for hydrogen production at most locations in the world. Moreover, the efficiency is impacted by the load-factor.

Hydrogen has been produced on large scale for many decades, with a total production in the world exceeds 100 Mt/a and with China as the largest producing country [29]. However, only a small fraction of the production is used outside of the chemical industries where it is produced. In general, hydrogen is rather difficult to distribute, and for larger demands it should preferably be produced onsite where it is to be used. Nevertheless, large industrial gases companies and others are distributing hydrogen both via pipeline networks and by using road tankers; some among them already operate more than 1,000 km of pipelines and over 1,600 road tankers [30] As was indicated in Figure 6, large-scale hydrogen production at a steel mill can also service a network of minor offtakers in the neighbourhood.

There are several issues with hydrogen that need to be taken into account when eyeing large-scale distribution of hydrogen, including, e.g., the small size of the hydrogen molecules, its low energy density, being flammable at low oxygen concentrations, hydrogen embrittlement. When moving into a future massive distribution and use of hydrogen, this needs to be further studied [31].

8 Conclusions

The steel industry can decarbonise significantly with hydrogen steelmaking, or CO2 capture and sequestration or use where feasible. However, these approaches are in general longer term (beyond year 2030) solutions that are not sustainable today due to the capital and operating cost impacts on steelmakers. For them to become sustainable or viable, we need a combination of higher costs of CO2 emissions, as well as a well-developed infrastructure to supply low-cost renewable power and hydrogen at very large scale. When viewing sustainability and carbon footprint, however, it is important to always consider the Scope 3 emissions, which can have various impacts; a great illustration is in the production and use of stainless steel where the vast majority of impact is found upstream in raw material supply chain whilst the impact over the life-cycle in use is very low [32].

Steelmakers can take short term steps with incremental and stepwise sustainable decarbonisation approaches that are affordable today. Energy efficiency improvements with oxyfuel combustion − with fossil fuel savings of 20–60% − offers immediate CO2 reductions with low CAPEX commitments on several unit processes. Proven oxyfuel based solutions can reduce the steel industry’s CO2 emissions by 200 Mt/a. Integrated steel mills can decarbonise by raising blast furnace tuyere injectant levels using external gasification, increasing the scrap ratio in converters, and by charging DRI/HBI produced by the gasification of low carbon footprint feedstocks and alternate fuels such as coke oven gas. When viable supply of hydrogen is available, there are many of opportunities to use it. Across the steel production process chains there are possibilities for use of hydrogen − as reductant or fuel − in many processes, including for example:

Blast furnace

DRI shaft

Electric Arc Furnace

Scrap cutting

Ladle preheating

Cutting at continuous casting

Reheat furnace

In the era of decarbonisation, we are now seeing moves towards both backward and forward integration of raw materials supply and use of gas-based DRI production in a much larger scale than previously. DRI would then substitute hot metal as a virgin raw material in the production of more advanced steel grades. Location of production is increasingly determined by viable availability of clean energy, which is due to the costs and difficulties to transport clean energy (including hydrogen) large distances; it is way more efficient to transport HBI or semi-finished steel products. These changes might lead to dislocations of existing value-chains.

References

- Statistics from World Steel Association, various production data updates published during 2022 and 2023 https://worldsteel.org/ [Google Scholar]

- Statistics from Midrex, various 2022 and 2023 editions of ‘Direct from Midrex’ xx xxxx https://www.midrex.com/direct-from-midrex/ [Google Scholar]

- https://www.eurofer.eu/publications/brochures-booklets-and-factsheets/european-steel-in-figures- 2022 / [Google Scholar]

- F. Patisson, O. Mirgaux, J.-P. Birat, Hydrogen steelmaking, part 1: physical chemistry and process metallurgy, Matériaux & Techniques 109 (3-4), 303 (2021) [Google Scholar]

- J.-P. Birat, F. Patisson, O. Mirgaux, Hydrogen steelmaking, part 2: competition with other net-zero steelmaking solution − geopolitical issues, Matériaux & Techniques 109 (3-4), 307 (2021) [Google Scholar]

- J. von Schéele, P.C. Mathur, Solutions for immediate and transition term decarbonization, in: Proc. 6th European Steel Technology and Application Days (ESTAD), 2023, Duesseldorf, Germany. [Google Scholar]

- A. Hauser et al., Valorizing steelworks gases by coupling novel methane and methanol synthesis reactors with an economic hybrid model predictive controller, Metals 12 (6), 1023 (2022) [CrossRef] [Google Scholar]

- A. Zaccara et al., Renewable hydrogen production processes for the off-gas valorization in integrated steelworks through hydrogen intensified methane and methanol syntheses, Metals. 10 (11), 1535 (2020) [CrossRef] [Google Scholar]

- I. Matino et al., Hydrogen role in the valorization of integrated steelworks process off-gases through methane and methanol syntheses, Matériaux & Techniques, 109 (3-4), 308 (2021) [CrossRef] [EDP Sciences] [Google Scholar]

- L. Deng et al., Techno-economic analysis of coke oven gas and blast 532 furnace gas to methanol process with carbon dioxide capture and utilization, Energy Conv. 533 Manag. 204, 112315 (2020) [CrossRef] [Google Scholar]

- B. Karlson et al., Commercializing LanzaTech, from waste to fuel: an effectuation case, J. Manag. Organ. 27 (1), 1–22 (2018) [Google Scholar]

- http://www.steelanol.eu/en [Google Scholar]

- A. Olsece et al., Reduction of gaseous emissions by applying a spray-scrubber-based process for cyanide compounds reduction in blast furnace gas, presented at AISTech 2023 − The Iron & Steel Technology Conference and Exposition, May 2023, Detroit (USA) [Google Scholar]

- P.C. Mathur, J. von Schéele, R.K. Nath, Solutions to decarbonize iron & steel making, Steel & Metallurgy, April, 2021 [Google Scholar]

- J. von Schéele et al., Hydrogen steelmaking − solutions for melting and reheating, Steel Times International, March, 2021, pp. 36–39 [Google Scholar]

- J.O. Edström, Järnsvampsprocesser, in: Järn- och stålframställning: utvecklingen i Sverige 1850 till 2000, Jernkontoret, 2004, pp. 126–153. [Google Scholar]

- I.N. Zaini et al., Decarbonising the iron and steel industries: production of carbon-negative direct reduced iron by using biosyngas, Energy Conv. Manag. 281 (11), 116806 (2023) [CrossRef] [Google Scholar]

- P.C. Mathur, J. von Schéele, Decarbonizing solutions for steel, Steel Times International, April, 2021, pp. 35–39 [Google Scholar]

- U. Zanusso et al., Development and testing of flameless burner fed by NG/H2 mix, Matériaux & Techniques 109 (3-4), 304 (2021) [Google Scholar]

- I. Luzzo et al., Feasibility study for utilization of natural gas and hydrogen blends on industrial furnaces, Matériaux & Techniques 109 (3-4), 306 (2021) [Google Scholar]

- A. Della Rocca et al., Rolling mill decarbonisation: Tenova Smartburners with 100% hydrogen, Matériaux & Techniques 109 (3-4), 309 (2021) [Google Scholar]

- P.C. Mathur et al., CoJet® − 25 years of revolutionizing EAF steelmaking, Steel Tech, Vol. 15, No. 4, July, 2021, pp. 65–71 [Google Scholar]

- W.J. Mahoney et al., The critical role of hydrogen in Linde’s coherent jet technology, Proceedings AISTech, 8–11 May, 2023, Detroit, USA [Google Scholar]

- J. von Schéele, Hydrogen flameless oxyfuel for CO2 free heating, Millennium Steel, May, 2021, pp. 32–35 [Google Scholar]

- J. von Schéele, Advancing Use of hydrogen as fuel in Steelmaking, Millenium Steel, May, 2022, pp. 20–22 [Google Scholar]

- J. von Schéele, H. Alshawarghi, D. Razzari, Technologies paving the way to carbon neutral stainless steel production, La Metallurgia Italiana, July/August, 2022, pp. 53–61 [Google Scholar]

- C. Nakkhong et al., Successful results from improved sustainability by using flameless oxyfuel in SYS, Proceedings 2019 Annual Meeting & Conference of South-East Asia Iron and Steel Institute (SEASI), June 16–19, 2019, Bangkok, Thailand [Google Scholar]

- J. von Schéele, Impact of decarbonisation on the steel industry structure, Green Steel World, April, 2023, pp. 28–31 [Google Scholar]

- J. von Schéele, From biggest in grey to biggest in green, Chapter on China in Touching Hydrogen Future − Tour Around the Globe, https://europeangasmarket.eu/ 157–172 [Google Scholar]

- https://www.lindehydrogen.com/ [Google Scholar]

- R. Valentini et al., Application of laboratory and on field techniques to determine the risk of hydrogen embrittlement in gaseous hydrogen and relative mixtures transport and storage, Matériaux & Techniques, 111 (2), 202 (2023) [CrossRef] [EDP Sciences] [Google Scholar]

- J. von Schéele, P. Samuelsson, Improving life-cycle of stainless steel: from start to finish, Stainless Steel World Americas, June, 2022, pp. 10–11 [Google Scholar]

Cite this article as: Joachim von Schéele, Pathways towards full use of hydrogen as reductant and fuel, Matériaux & Techniques 111, 405 (2023)

All Figures

|

Fig. 1 The transition into low-carbon footprint steelmaking with near-term activities, multiple solutions, and long-term development projects. |

| In the text | |

|

Fig. 2 The hot oxygen technology can support a circular economy using gasification to produce low-carbon footprint syngas for ironmaking processes. |

| In the text | |

|

Fig. 3 CoJet flame shrouding with an oxyfuel flame around the oxygen jet. |

| In the text | |

|

Fig. 4 Flameless oxyfuel using 100% hydrogen as fuel at world’s first full-scale test of steel reheating with all hydrogen combustion in March 2020 at Ovako Steel in Sweden. |

| In the text | |

|

Fig. 5 CO2 emission cost versus cost of hydrogen (and electricity) providing areas where hydrogen-based steel is favourable and not. |

| In the text | |

|

Fig. 6 Outline of integrated green steel production ecosystem for a 2 Mt/a DRI-EAF steel plant with 100% green hydrogen and oxygen. |

| In the text | |

Current usage metrics show cumulative count of Article Views (full-text article views including HTML views, PDF and ePub downloads, according to the available data) and Abstracts Views on Vision4Press platform.

Data correspond to usage on the plateform after 2015. The current usage metrics is available 48-96 hours after online publication and is updated daily on week days.

Initial download of the metrics may take a while.