")

")

| Issue |

Matériaux & Techniques

Volume 112, Number 6, 2024

Special Issue on ‘From Advanced Technology to Social Sciences, how to bring materials development into the Ecological Transition? ’, edited by J.P. Birat, A.L. Hettinger, A. Declich, L. Kolbeinsen, A. Jo, J.R. Gyllenram, A. Jarfors

|

|

|---|---|---|

| Article Number | 605 | |

| Number of page(s) | 12 | |

| Section | Metals and alloys | |

| DOI | https://doi.org/10.1051/mattech/2025005 | |

| Published online | 09 April 2025 | |

Original Article

Functionally integrated castings (Giga-castings) for body in white applications: consequences for materials use and mix in automotive manufacturing

Jönköping University, School of Engineering, Materials and Manufacturing, Box 1026, 551 11, Jönköping, Sweden

* Corresponding author: This email address is being protected from spambots. You need JavaScript enabled to view it.

Received:

10

June

2024

Accepted:

23

February

2025

Abstract

Three significant changes are driving the use of materials in the automotive industry today. First, the direct environmental load of materials drives the issue of climate change through the associated carbon footprint of the car from manufacturing to use and end-of-life phases. The new consumer attitudes and legislation force new requirements on the automotive industry. These requirements constitute the second driver, pushing the electrification of the drive line and the use of batteries. The electrification significantly simplifies the car’s architecture and allows for a more significant functional integration of the automotive components. This leads to functional integration in component design, considerably changing the conditions to the third driver, consisting of reduced raw material use, material efficiency and recycling and how to achieve cost-effectiveness and resource efficiency. Closing the circle to the climate impact and the carbon footprint changes dramatically. The current paper reviews and analyses the consequences of electrification and the use of Giga casting on aluminium alloys, especially alloying element streams, for recycling in the automotive industry, targeting a near-closed-loop approach. This analysis is made to identify potential resource quality and availability issues for the aluminium alloys and the alloying elements used. It was concluded that there would be a significant need for primary or non-automotive aluminium scrap to be introduced into the flow. All electrified drivelines will allow for a closed-loop scenario where Mg, Si and Mn are the first to reach surplus and Fe, Zn, and Cu are the last. Critical is that the additions of Si made in the recycling process can, in theory, be eliminated. Si is responsible for more than half the carbon footprint of aluminium alloy recycling.

Key words: Automotive / functional integration / cast component / climate change / materials usage

All authors contributed equally to this work.

© A.E.W. Jarfors et al., 2025

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

1 Introduction

Tomlinson et al. [1] issued scientists warnings on technology, concluding that:

Current technologies are causing profound environmental and social harm.

It is important to remain vigilant for potential future harm and reduce it as much as possible.

More broadly, Sustainable futures require profound cultural, political, and societal shifts.

Technology change will be integral to working towards that goal.

Understanding that Tomlinson et al. [1] stated that technology is both part of the problem and the solution opens a significant impact by technology on managing climate change and the resulting total greenhouse gas emissions [2]. The fact that technology is both the root of the problem and part of the problem should be contextualised in the way it is being applied from a systemic perspective. This means that the main issue is not technology itself but rather how we apply technology. In the transport industry, such as the automotive industry, lightweight has been seen as a critical element in reducing carbon footprint in transitioning from a fossil-based energy system to an electricity-based fossil-free system. The overall weight of cars for the actual energy consumption is critical for reducing emissions, especially early on when the dependence on fossil-fuel-based electricity is significant [3]. The transformation of the energy supply for the automotive industry makes a substantial impact on the total climate impact by Röyne and Bolin [4], illustrating that as the energy supply system changes from a fossil-based system to a green energy system, the tonne of carbon dioxide equivalents (CO2e) for a car such as Volvo XC40 with internal combustion with 58 tonne CO2e during manufacturing and use reduces to 25 tonne CO2e for a fully electric standard version of Polestar 2 with wind energy as a source of electricity. Almost all of the remaining 25 tonnes of CO2e originate from the materials used in the car. The carbon emission from the materials fabrication and generation is thus, even with complete electrification, a major issue.

To address this, one proposed approach is to recognise that a sustainable transformation is a process that requires a framework to reach a sustainable future that minimises emissions, efficiently uses resources, and provides a sound and functional life for humans. This approach would encompass the following [5]:

System: defining its constitution and the rules.

Success: Having a vision to be framed by basic sustainability principles.

Strategic guidelines: How to approach the principle-framed vision strategically using stepwise transitions.

Actions: Education, use of materials, energy sources, working conditions.

Tools: Sustainability modelling, simulation, life cycle assessment, management systems, and indicators supporting stepwise change.

From the European perspective, the European Aluminium Organisation formulated the following five priorities for the European aluminium industry for the period of 2024–2029 [6]:

Effective industrial strategy.

Boost a green transition “Made in Europe”.

Competitive energy prices and support industrial decarbonisation.

Revitalised trade defence and policy.

A substance management framework that builds on coherent environmental practices.

The automotive industry is greatly affected by electrification, which significantly changes the car’s architecture and how it is being fabricated. These changes may have profound implications for the material producers and the recycling industry. One effect in particular is a significant increase in the use of aluminium alloys, especially wrought aluminium [7–12]. Billy and Müller [9] reported that the use of aluminium (Al) will increase fourfold from 2020 to 2050, primarily driven by the electrification of the automotive vehicle fleet.

In the automotive industry, recycling follows a downcycling procedure from wrought to cast alloy components. This practice is resource waste as it often requires dilution and silicon (Si) additions, with increased energy consumption and carbon footprint related to the latent heat of fusion of the scrap mix [11,13].

The need for downcycling is strongly associated with the wrought alloys’ sensitivity to impurity elements [11], impairing product quality and processability. This sensitivity caused alloying friction and a matching issue, causing a global scrap surplus that will tend to grow unless better sorting and recycling are developed [12].

An increased use of wrought alloy may make recycling and alloy matching more difficult in recycling due to their unforgiving nature. This difficulty is associated with an increased usage of wrought materials in BEVs. There are projections that the CO2 emissions from aluminium in vehicles will drastically increase and exceed those of the battery materials such as nickel, lithium, cobalt and manganese (Mn), again attributed to the increased surplus of scrap that cannot be utilised for wrought products [9].

The introduction of Giga and Mega casting processes is changing the landscape for automotive companies, where a significant reduction in material numbers is achieved, including steel sheets being replaced by aluminium castings [14]. In addition, there are benefits, such as increased potential for using recycled materials with reduced sensitivity of impurities and broader specification associated with cast alloys. This may open up the chemical composition specifications and ease of alloy matching to digest the scrap surplus and improve the effectiveness of aluminium scrap recycling and usage.

The current paper reviews and analyses the consequences of electrification and the use of Giga casting on aluminium alloys and alloying element streams for recycling in the automotive industry. The aim is to understand the possibilities and conditions for a closed or near-closed loop recycling scenario for the automotive industry. This analysis is made to identify potential resource quality and availability issues for the aluminium alloys and the alloying elements used.

2 Material and methods

The current work has the foundation in literature and automotive market data. The idea is to produce an upper and lower bound estimate for the evolution of the automotive market growth to achieve an alloying element balance. The purpose is to understand if conditions are suitable for a closed-loop scenario based on the overall change in aluminium usage, driven by electrification, the changes in how a car is built, and the associated processes used.

The first step in achieving a mass balance was to use market data to establish an upper and lower bound for the automotive market evolution based on the following assumption.

The first upper bound material usage with business as usual and extrapolation as an upper bound estimate.

The second lower bound material usage with a reduced car market expansion with compensation for the increase of the car lifespan after 2022 as a lower bound estimate.

Data on a car’s weight evolution is necessary to estimate the aluminium alloy usage. Cars have been growing larger and heavier, driven by passive safety measures, and there has been a general growth in size with the introduction of sports utility vehicles (SUVs) and so forth. The assumptions made here were that an average car weight would be sufficient to estimate the material usage, and the actual mix of the car types and models would be implicitly included in the evolution of weight. To achieve a robust estimate, several different fitting methods were tested, estimating the evolution of the car’s weight to get the total mass of the vehicles being produced, including linear, logarithmic, exponential and power law models. Since the aim was an extrapolation, higher-order polynomials were excluded as the extrapolation depends on the sign of the highest-order term coefficient and would ne be considered robust. The model choice was then made based on the best R-squared value. The same process was made for the amount of aluminium alloys used in cars, and this amount was reasonably equal worldwide, ranging from 7.2% to 9.3% in 2017. More interesting was that the vehicles with the highest aluminium contents were found in the US, Western and central Europe, Japan and China [15]. These regions also dominate the markets for car production and sales.

Estimating the amounts of alloying elements used in the automotive industry requires three scenarios. The first scenario is business as usual, using an ICE with zero BEV introduction as the baseline. This serves as a baseline for comparison to the other scenarios. The changes that may allow closed-loop recycling were based on the automotive fleet’s ongoing electrification. For the aluminium alloys, this means a change in the type of alloy used, and the mass balance will depend on the number of cars made and the market penetration of BEVs. The market penetration of BEV was assumed to follow logistic regression, assuming that all cars will eventually be BEV. This is naturally a questionable argument. However, the market share ratio between hybrid vehicles and BEVs is decreasing, and it is similar to other alternatives, including hydrogen-based solutions, making BEVs the dominant and most viable solution [16]. The three different scenarios were constructed as follows:

Extrapolation of today’s ICE market as a reference;

The extrapolation of today’s EV scrap is being returned for 100% recycling using a market penetration based on logistic regression;

Extrapolation of today’s EV scrap with a Mega casting usage being returned for 100% recycling.

For the EV scenario and the EV and Giga/Mega casting scenario, the level of aluminium usage is the same as the actual material replacement scenario, and effects only have a few examples and no reliable data other than what was published by Rolseth et al. [17]. In the work by Rolseth et al. [17], the overall mass balance change from the replacement of steel to aluminium was not taken into account, but assuming that aluminium was replaced by aluminium, making the effect on the replacement of cast alloys to wrought alloys slightly exaggerated.

To make a mass balance, the average composition of the car was returned as shredded, and material-separated scrap was assumed. This corresponds to cleaned and separated Zorba class aluminium scrap (according to the ISRI standard) [18]. This chemistry naturally varies over time and by batch, but an average is possible for ICE and EVs [19]. This results in three different scenarios for the chemical composition of the scrap:

ICE chemistry, which is the baseline;

BEV chemistry, which depends on the market penetration of BEVs and displaces the ICE chemistry;

BEV and Giga/Mega casting chemistry depend on the BEV market penetration, displacing the ICE chemistry.

The penetration rate of Giga/Mega casting is not considered, but its consequence is to be judged by the difference between the two non-ICE scenarios.

The material being fed back as scrap is the end-of-life of the material and is affected by the lifespan of the car as it is an old chemistry that is being returned; therefore, the lifespan of the cars was used to represent the lag in chemistry change that this would represent.

3 Results

3.1 Automotive market evolution

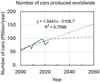

The evolution of cars varies from year to year, and the economic instability before 2010 and the COVID-19 pandemic in 2020 have reduced the number of cars produced in the post-pandemic period. Production and sales appear to have recovered [20]. Taking a linear regression as a first estimate of the number of cars, NA, as expressed in Equation (1):

(1)

(1)

where aN and bN are constants and ty is the year. The fitted values and the lifespan compensated extrapolation are shown in Figure 1 as the dotted and dashed lines, respectively.

There are naturally significant uncertainties in this estimate. Based on consumer behaviour insights from the last few years, several uncertainties are driven by cost levels, new technology, the transition to electric vehicles, and all related uncertainties. Market research by Deloitte Development LLC [22] indicates that the following matters related to the transition to electric vehicles drive the uncertainty:

The consumers’ willingness to pay for advanced technologies;

Concerns about price, driving range, and charging time remain;

The shift to EVs is primarily based on a strong consumer perception that it will significantly reduce vehicle operating costs.

The operating cost depends on the energy price and the funding model for car ownership. Furthermore, changing the possible car owner models will affect the overall ownership costs. De Jong et al. [23] studied the new car ownership model developed after 1995, which was used to evaluate transport needs.

The car ownership models for electric vehicles commonly involve subscription services. The three main reasons for the use of a subscription service include:

Convenience;

Complete cost control due to transparent and predictable fixed monthly fees;

Availability of vehicles.

The main concerns for the use of a subscription service are:

Vehicle availability/waiting time;

Total cost of ownership (i.e., price);

Losing the sense of ownership;

Higher monthly fees compared to leasing.

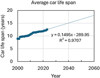

All these uncertainties combined will also require a decreased demand perspective for the current analysis. This is also motivated by the variations seen in the evolution of the market, with more significant dips in sales just before 2010 and after 2020. These changes in consumer behaviour and ownership models combined with the slowly increasing life span for cars, in Figure 2, suggest that a reduced number of cars can provide a sufficient service for the transport needs of society. In the current study, the increased life span of the cars will be used to provide a car lifespan compensated by market evolution. The continued growth and the lifespan compensated growth will be used to estimate the overall material demands in the automotive industry as an upper and lower bound, respectively. Similarly, the effect of battery life is unclear. Therefore, it is assumed that this effect is implicitly included in the lifespan data, but its specific impact must be considered. Using data from Statista [21], the life span of a car, LA, is expressed in Equation (2):

(2)

(2)

where aL and bL are constants and ty is the year. The fit is shown by the dotted line in Figure 2.

The number of cars was normalised to make the life span compensation, as per equation (3).

(3)

(3)

The compensated number of cars,  is shown in Figure 1 as the dashed line and indicates a significant reduction and, as such, a conservative estimate of the market evolution.

is shown in Figure 1 as the dashed line and indicates a significant reduction and, as such, a conservative estimate of the market evolution.

To estimate the amount of aluminium in a car, it is necessary to have the average car mass and the average aluminium content of cars. The linear model provided the best fit based on the R-squared value among power law, exponential and logarithmic models. Hence, a linear model was chosen and the average weight of a car, MA, worldwide is then expressed by equation (4):

(4)

(4)

where aM and bM are constants and ty is the year. The fit to data by Cazzola et al. [24] is shown in Figure 3.

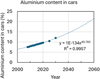

As an estimate, the average amount of aluminium in a car as weight per cent, FAl, was extracted from data from Statista [25]. The choice of type of equation for the modelling was based on the fitting statistics where the power law model had the highest R-squared value. The model used is thus expressed as equation (5):

(5)

(5)

where aF and bF are constants and ty is the year. The fit, using data from Statista [25], is shown in Figure 4.

|

Fig. 1 The number of cars produced per year (solid line) and two scenarios: linear extrapolation of the market data [20] (dotted line) and lifespan compensation using vehicle lifespan data [21] and the model developed for life span together with linear market evolution model (dashed line). |

3.2 Automotive market, electrification and Giga/Mega casting

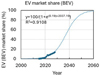

Electrification of the automotive market comes in different types. The current study assumes that it is necessary to include only battery electric vehicles (EVs) based on market data for different fuel systems [16]. The change is taking place at an increasing rate, and the market penetration, FE, is modelled as an S-shaped logistic function as in equation (6):

(6)

(6)

where aE and bE are constants and ty is the year. The fit to the existing data [26] is shown in Figure 5.

The effect of electrification on the average compositions of the aluminium in cars was analysed by Rolseth et al. [17]. Table 1 shows the average scrap composition,  , for element i and scenario S. Rolseth et al. [17] concluded that the average composition of aluminium depends on the relative usage of cast and wrought materials, where alloys for Mega-casting have a lower Si-content than traditionally used alloys in the automotive industry. Wrought alloys have, in general, much lower amounts of alloying elements, such as Si, when compared to cast alloys. It is, therefore, assumed that the scrap composition is a significant fingerprint of the actual aluminium usage in the different types of cars, as summarised by Rolseth et al. [17].

, for element i and scenario S. Rolseth et al. [17] concluded that the average composition of aluminium depends on the relative usage of cast and wrought materials, where alloys for Mega-casting have a lower Si-content than traditionally used alloys in the automotive industry. Wrought alloys have, in general, much lower amounts of alloying elements, such as Si, when compared to cast alloys. It is, therefore, assumed that the scrap composition is a significant fingerprint of the actual aluminium usage in the different types of cars, as summarised by Rolseth et al. [17].

The mass of each element, i, for the different scenarios S can be calculated starting with the total amount of aluminium alloys used for cars, MAl, equation (7).

(7)

(7)

For the scenario with a straight extrapolation of the car life span and the life span compensated scenario, this becomes equation (8).

(8)

(8)

Consequently, it is possible to calculate the mass of the different alloying elements used in the cars for the various scenarios in equation (9).

(9)

(9)

The demand for recycled alloying elements in scrap on a worldwide basis in an automotive closed recycling loop,  , for the year, ty, would then be the same as that of equation (9). This can be expressed as equation (10).

, for the year, ty, would then be the same as that of equation (9). This can be expressed as equation (10).

(10)

(10)

The supply,  , on the other hand, would be the mass demand. LA years before, as in equation (11).

, on the other hand, would be the mass demand. LA years before, as in equation (11).

(11)

(11)

The alloying element discrepancy or supply and demand gap for element i,  in the year ty is then expressed in equation (12).

in the year ty is then expressed in equation (12).

(12)

(12)

The impact of the BEV market penetration, FE in equation (13), is difficult to judge as the amount or mass of aluminium is increased in the BEV, but there is also a tendency for an increased weight of the cars, and therefore, it is hard to estimate the effect on FAl in the cars at this early stage of the transition. To some extent, the early trends can be seen as implicitly included in the mass evolution of the cars and the increase of the relative amount of aluminium in the cars, FAl. This study focuses on the chemical composition of the aluminium alloys, which has been analysed and used as input for the material balance. The market penetration of the EV into the ICE market has not yet been included, as summarised in Equation (13). The three scenarios are ICE for the combustion engine scenario, EV is the electric vehicle only, and EVM is the EV + Mega casting class.

(13)

(13)

|

Fig. 5 The evolution of the EV market share over time and the predicted evolution using logistic modelling based on market data [26]. |

4 Discussion

4.1 Material balances

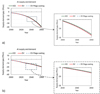

The first element of the balance of interest is that of aluminium. The growing number of cars will require an increased amount of material based on the increased weight and amount of aluminium in the cars. This is shown in Figures 6a and 6b for the continued automotive demand and the lifespan compensated demand, respectively. For both market scenarios, aluminium is not a base element. Adding primary or non-automotive scrap aluminium to the closed-loop scenario is necessary to balance supply and demand. The requirements are slightly lower for the reduced market growth, the lower bound, Figure 6b, than for the continued growth or upper bound, Figure 6a. There is a slight difference in the need for aluminium for the two estimates, originating from the elements’ net balance. The ICE average composition is the lowest on aluminium, and Si is the dominant alloying element. This balance is also reflected in the other two scenarios, with the EV only having the greatest need for aluminium as it is the leanest in alloying concentrations. The continued negative balance for aluminium will require the addition of aluminium, either virgin for or as scrap, from outside sources to the automotive material flows. This may introduce other impurities, and there may be a concern about copper (Cu) contamination from electronic scrap.

In conclusion, a fully closed recycling solution will not be possible under current estimated consumption scenarios, and aluminium additions to the material flow will be required.

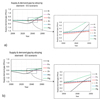

The situation is very different for the other alloying elements under a closed-loop scenario. Starting with the outcome of the analysis of the ICE scenario where there is no significant change in the alloying composition but only in the use of the aluminium, this is bound to follow a similar trend as the aluminium use. This is also seen in the continued growth market estimated results, Figure 7a and the life span compensated estimate, Figure 7b. It should be noted that this is a significant simplification as the increased use of aluminium also involves a slight change in the types of alloys being used, and the assumed composition is a reasonable assumption but crude for a quantitative actual prediction. Reaching any steady state without a transition to EV can, however, be deemed impossible, and there will be a constantly increasing need for the use and addition of virgin elements into the system, and a fully scrap-based alloying approach is not possible.

The change to the use of a fully electrified drive line has a prominent impact on the use of alloys. The need for aluminium will increase slightly but dramatically change the alloying element balance in the demand and supply for aluminium alloys, Figures 8a and 8b. For both scenarios, there is a minimum point followed by an excess for all materials. This suggests that a closed-loop scenario is possible as the scrap will supply more of the main alloying elements than is needed. The sequence is of interest, where magnesium (Mg) is the first element that goes into excess, followed by Mn, iron (Fe), zinc (Zn), Si, and last Cu. The fact that Mg comes first is significant due to supply-chain resilience issues and the critical raw materials status [28]. A reduced market growth reduces the amplitude of the curves and slows the transition towards balance, making the process take longer. The difficulty here is the element matching, as the EV-only scenario includes mainly wrought alloys that are more difficult to produce based on the post-consumer scrap. It is thus likely that the net balance cannot be reached without a significant surplus of elements. The level of this limit is unknown, but the analysis shows that, in principle, it should be more feasible to close the scrap loop supporting a producer take-back principle. This is more likely with increased materials traceability and product passport solutions that also are likely to lower the critical threshold to reach a producer take back scrap systems approach.

Introducing Mega or Giga casting into car manufacturing significantly reduces automotive producers’ costs. In the current work, Mega or Giga casting has not been considered to impact the aluminium content in the cars even though steel parts are replaced by aluminium castings, as commented above. This suggests that the use of aluminium is slightly underestimated in this scenario. The supply and demand balance for the two scenarios are shown in Figures 9a and 9b. Mega or Giga casting will also reach a positive supply balance for the elements. The sequence is similar to the EV scenario, with Mg being the first element that goes into a situation of excess, followed by Mn. Giga or Mega casting causes Si to come into excess earlier, followed by Zn, Fe and Cu delays. Cast alloys generally have broader functional composition ranges than extruded or rolled products. These characteristics suggest that it should be easier to close the loop with an increased use of cast components than with a scenario involving extrusions and sheets only [11].

|

Fig. 6 The supply and demand balance for aluminium for different scenarios: a) the continued growth scenario and b) the lifespan compensated scenario. |

|

Fig. 7 Material balance for the benchmark ICE with a) continued growth and b) lifespan-compensated growth. |

|

Fig. 8 The effect of the material balance for the EV scenario with: a) continued growth, showing the shift to element surplus in the scrap with continued growth with a transition to EVs, and b) the evolution with a lifespan compensated growth with a similar shift for the continued growth. |

|

Fig. 9 The effect of the material balance for the EV and Mega casting scenario with: a) continued growth, showing a shift to element surplus in the scrap with continued growth, b) the evolution with a lifespan compensated growth showing a similar shift in the supply and demand situation. |

4.2 Climate impact

The main issue for aluminium recycling is the material balance and the use of high Si-containing materials in downgrading and recycling alloys to cast alloys. Material downgrading has been used for component casting in the aluminium recycling business, particularly engine block castings with high Si content and significant Cu and Fe content. These alloys provide strength but have very limited ductility and, as such, cannot be used in components that require fatigue resistance and crashworthiness [11,29]. Another feature is that alloys with 9% Si or more need significant additions of virgin Si. This builds in an energy hysteresis in the recycling system, making it much more energy-consuming, but foremost, it also represents a significant carbon footprint increment with 10.9 kgCO2/kgSi [30]. In 2022, this increment corresponded to 4.7 Mton based on the ICE model. The evolution of the carbon footprint for the different scenarios is found in Figure 10a for the continued market growth and in Figure 10b for the lifespan compensated growth. It is evident that, independently of market growth, the continued evolution based on ICE drivelines alone will only increase the contribution to global carbon emissions.

On the other hand, the Si balance has a significant impact as it is a direct consequence of the Si balance in the recycling loop. Both market growth cases suggest a peak around 2030 and neutrality around 2040 if a closed loop scarp cycle could be achieved with a reduced Si content and allowing the alloying and reuse of scrap to be the source of alloying elements. On the other hand, this requires an improved ability among cast houses and foundries to make their alloys adapt to new situations and adopt different approaches to alloying. The critical element in this analysis is to enable alloys with a lower amount of Si, allowing the current scrap to be recycled and used as a source of Si. This shift in practice leads to discontinuing downcycling with dilution and adding Si to conventional wrought alloys to reach the high Si content of cast alloys. The aim should be to try to use and adapt to allow the adoption of alloys more similar to the aluminium returned as Zorba class scrap.

|

Fig. 10 The carbon footprint evolution from the added silicon (Si) contribution in a closed loop circular material situation for the automotive industry for the three scenarios discussed: a) continued growth of the automotive market and b) lifespan compensated growth. |

5 Conclusion

The current paper investigated the hypothetical scenario of a closed-loop materials flow for the automotive industry. This was made to understand better the element balance related to alloying requirements and all related matters, such as availability, resilience, and climate impact.

The investigation shows clearly that under the two market growth scenarios constructed to generate an upper and lower bound market estimate, there will be an accelerated use of all alloying elements and virgin materials are constantly required to make a closed-loop balance, meaning that materials are needed to be taken from other material flows. This may, as such, result in contamination issues from different types of materials mixes. In the same line of investigation, there will be a need to add virgin or scrap aluminium from outside the automotive material flows with similar complications. This outcome was independent of the market growth and the choice of manufacturing route. The increased usage of wrought materials increases the need for aluminium addition to the loop as the alloys contain fewer alloying elements than the cast alloys used in the ICE cars. This stresses the need for better sorting and recycling solutions and supports the findings by Van den Eynde et al. [12]. The sensitivity to oxide impurities, chemical elements such as Fe, and other scrap-related impurities significantly and detrimentally affect aluminium alloys’ mechanical and electrochemical/corrosion properties [11]. The consequence of contaminations makes it preferred from a materials performance standpoint to have closed loops, especially for the automotive industry and safety requirements [29,31].

Comparing the three scenarios, the change from ICE to EV reveals that the first evident matter to note is that no conditions lead to an alloying element surplus for the ICE scenario, and any closed-loop scenario is impossible.

In the EV scenario, alloying elements will come into an excess balance. An element surplus could enable a balanced closed loop with only additions of aluminium from outside sources. An actual balance will likely require excess availability, as balancing between alloys will be required. The EV-only solution would primarily involve wrought alloys and the extra challenges associated with recycling.

Adding Mega / Giga casting to the material mix allows quicker balancing, particularly for Si as an alloying element. It was argued that Mega casting would make recycling easier as casting is a well-established route for recycled materials and has a history of being more forgiving towards trace elements through broader composition specifications.

The climate impact is primarily driven by the additions of Si to current recycling. The balancing of Si in a closed loop scenario will rapidly reduce the need for the additions, and the analysis suggests that it is possible with the EV transition and Mega casting to minimise the need for addition and the resulting emissions from additions of virgin Si during recycling to zero before 2040 with a closed loop approach.

Acknowledgments

The authors thank Jean-Pierre Birat from IF Steelman and Rutger Gyllenram from Kobolde and Partners for inspiring the start of this analysis.

Funding

Vinnova funded the current paper through the projects ClimAl (contract 2022-02602) and KlirAl (contract 2022-00819).

Conflicts of interest

The authors declare no conflict of interest.

Data availability statement

The data used for market estimates are given in the appendix.

Author contribution statement

AJ secured the funding, conceptualised, and wrote the first draft. LL reviewed the work and provided feedback and advice on the modelling and presentation. TB provided input and support on the modelling work. AJ, LL and TB all approved the final version.

References

- B. Tomlinson, A.W. Torrance, W.J. Ripple, Scientists’ warning on technology. J. Clean. Prod. 434 (2024). doi:10.1016/j.jclepro.2023.140074 [CrossRef] [Google Scholar]

- H. Ritchie, P. Rosado, M. Roser, CO₂ and Greenhouse Gas Emissions. Available online: https://ourworldindata.org/co2-and-greenhouse-gas-emissions (accessed on May 28, 2024). [Google Scholar]

- A.C. Serrenho, J.B. Norman, J.M. Allwood, The impact of reducing car weight on global emissions: the future fleet in Great Britain, Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 375, 20160364 (2017) [CrossRef] [Google Scholar]

- F. Røyne, L. Bolin, Life cycle assessment 2021-carbon footprint of Polestar 2 variants (2020) Available online: https://www.polestar.com/dato-assets/11286/1630409045-polestarlcarapportprintkorr11210831.pdf (Accessed on March 16, 2025) [Google Scholar]

- G.I. Broman, K.H. Robèrt, A framework for strategic sustainable development, J. Clean. Prod. 140, 17–31 (2017) [CrossRef] [Google Scholar]

- European Aluminium 5 Priorities 2024–2029 (2024) Available online: https://european-aluminium.eu/wp-content/uploads/2024/02/European-Aluminium-5-key-policy-priorities-for-2024-2029.pdf (accessed on March 16, 2025) [Google Scholar]

- Ducker Worldwide Aluminum Content in Cars (2016) Available online https://www.alfed.org.uk/files/Fact%20sheets/european-aluminium-ducker-study-summary-report_sept.pdf (accessed on March 16, 2025) [Google Scholar]

- Ducker Frontier Aluminum Content in European Passenger Cars. Eur. Alum. 2019, 13. [Google Scholar]

- R.G. Billy, D.B. Müller, Aluminium use in passenger cars poses systemic challenges for recycling and GHG emissions, Resour. Conserv. Recycl. 190, 106827 (2023) [CrossRef] [Google Scholar]

- R. Modaresi, A.N. Løvik, D.B. Müller, Component- and alloy-specific modeling for evaluating aluminum recycling strategies for vehicles, J. Mater. 66, 2262–2271 (2014) [Google Scholar]

- D. Raabe, D. Ponge, P.J. Uggowitzer, M. Roscher, M. Paolantonio, C. Liu, H. Antrekowitsch, E. Kozeschnik, D. Seidmann, B. Gault et al., Making sustainable aluminum by recycling scrap: the science of “dirty” alloys, Prog. Mater. Sci. 128, 100947 (2022) [CrossRef] [Google Scholar]

- S. Van den Eynde, E. Bracquené, D. Diaz-Romero, I. Zaplana, B. Engelen, J.R. Duflou, J.R. Peeters, Forecasting global aluminium flows to demonstrate the need for improved sorting and recycling methods, Waste Manag. 137, 231–240 (2022) [CrossRef] [Google Scholar]

- Jarfors, A.E.W.; Jansson, P. Selecting Cast Alloy Alloying Elements Suitable for a Circular Society. Sustainability 2022, 14, 6584. Doi: 10.3390/su14116584 [Google Scholar]

- D. Carney, Tesla’s Switch to Giga Press Die Castings for Model 3 Eliminates 370 Parts, Design News; 2021. Available online: ww.designnews.com/automotive-engineering/teslas-switch-giga-press-die-castings-model-3-eliminates-370-parts ( accessed on Feb 27, 2023) [Google Scholar]

- M. Placek, Aluminum share in medium-sized passenger cars in 2017, by region. Available online: https://www.statista.com/statistics/886426/aluminum-share-in-medium-sized-passenger-cars-by-region/ (accessed on Oct 21, 2024). [Google Scholar]

- Statista Passenger Cars − Worldwide. Available online: https://www.statista.com/outlook/mmo/passenger-cars/worldwide?currency=USD (accessed on Oct 7, 2024). [Google Scholar]

- A. Rolseth, M. Carlsson, E. Ghassemali, P. Lluís, E. Anders, Impact of functional integration and electrification on aluminium scrap in the automotive sector: a review, Resour. Conserv. Recycl. 205 (2024). doi:10.1016/j.resconrec.2024.107532 [CrossRef] [Google Scholar]

- ISRI Shredded Nonferrous Scrap (predominantly aluminum). Available online: https://www.isrispecs.org/orpheus_resource/shredded-nonferrous-scrap-predominantly-aluminum/ (accessed on Oct 7, 2024) [Google Scholar]

- P. Krall, I. Weißensteiner, S. Pogatscher, Recycling aluminum alloys for the automotive industry: Breaking the source-sink paradigm, Resour. Conserv. Recycl. 202 (2024). doi:10.1016/j.resconrec.2023.107370 [CrossRef] [Google Scholar]

- M. Placek, Estimated worldwide motor vehicle production from 2000 to 2023. Available online: https://www.statista.com/statistics/262747/worldwide-automobile-production-since-2000/. [Google Scholar]

- M. Carlier, Average age of light vehicles in operation in the U.S. from 2002 to 2021 Available online: https://www.statista.com/statistics/185198/age-of-us-automobiles-and-trucks-since-1990/ (accessed on May 28, 2024) [Google Scholar]

- Deloitte Development 748 Q3 LLC. Global Automotive Consumer Study 2024 (2024). Available online https://www2.deloitte.com/content/dam/Deloitte/pe/Documents/consumer-business/gx-deloittes-2024-global-automotive-consumer-study-january.pdf (accessed on March 16, 2025) [Google Scholar]

- G. de Jong, J. Fox, A. Daly, M. Pieters, R. Smit, Comparison of car ownership models, Transp. Rev. 24, 379–408 (2004) [CrossRef] [Google Scholar]

- P. Cazzola, L. Paoli, J. Teter, Trends in the Global Vehicle Fleet 2023: Managing the SUV Shift Transition and the EV Transition Q4 (2023) Available online: https://www.globalfueleconomy.org/media/792523/gfei-trends-in-the-global-vehicle-fleet-2023-spreads.pdf (accessed on March 16, 2025) [Google Scholar]

- Statista Research Department Share of curb weight of medium sized cars produced in Western Europe attributable to aluminum from 2008 to 2030. Available online: https://www.statista.com/statistics/897794/western-europe-aluminum-as-share-of-car-curb-weight/ [Google Scholar]

- M. Carlier, Global market share of electric vehicles within passenger car sales between 2010 and 2022. Available online: https://www.statista.com/statistics/1371599/global-ev-market-share/ (accessed on May 28, 2024) [Google Scholar]

- European Parliament. EU ban on the sale of new petrol and diesel cars from 2035 explained Available online: https://www.europarl.europa.eu/news/en/headlines/economy/20221019STO44572/eu-ban-on-sale-of-new-petrol-and-diesel-cars-from-2035-explained (accessed on May 29, 2024) [Google Scholar]

- European Commision COM(2020) 474 final. Critical Raw Materials Resilience: Charting a Path towards greater Security and Sustainability EN Q5 (2022) Available online https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0474 (accessed on March 16, 2025) [Google Scholar]

- M. Tiryakioğlu, A.E.W. Jarfors, M. Leitner, The impact of the minimum ductility requirement in automotive castings on the carbon dioxide footprint throughout the useful life of an electric car, Metals (Basel) 13, 513 (2023) [Google Scholar]

- Ansys® Granta Selector 2023 R1; ANSYS, Inc. [Google Scholar]

- S.K. Das, Designing aluminum alloys for a recycling friendly world, Mater. Sci. Forum 519-521, 1239–1244 (2006) [CrossRef] [Google Scholar]

Cite this article as: Anders E.W. Jarfors, Toni Bogdanoff, Lucia Lattanzi, Functionally integrated castings (Giga-castings) for body in white applications: consequences for materials use and mix in automotive manufacturing. Matériaux & Techniques 112, 605 (2024) https://doi.org/10.1051/mattech/2025005

All Tables

All Figures

|

Fig. 1 The number of cars produced per year (solid line) and two scenarios: linear extrapolation of the market data [20] (dotted line) and lifespan compensation using vehicle lifespan data [21] and the model developed for life span together with linear market evolution model (dashed line). |

| In the text | |

|

Fig. 2 The average life span of a car [21]. |

| In the text | |

|

Fig. 3 The average weight of a car based on global data, including EV [24]. |

| In the text | |

|

Fig. 4 Cars’ aluminium content (wt.%) as a share of curb weight [25]. |

| In the text | |

|

Fig. 5 The evolution of the EV market share over time and the predicted evolution using logistic modelling based on market data [26]. |

| In the text | |

|

Fig. 6 The supply and demand balance for aluminium for different scenarios: a) the continued growth scenario and b) the lifespan compensated scenario. |

| In the text | |

|

Fig. 7 Material balance for the benchmark ICE with a) continued growth and b) lifespan-compensated growth. |

| In the text | |

|

Fig. 8 The effect of the material balance for the EV scenario with: a) continued growth, showing the shift to element surplus in the scrap with continued growth with a transition to EVs, and b) the evolution with a lifespan compensated growth with a similar shift for the continued growth. |

| In the text | |

|

Fig. 9 The effect of the material balance for the EV and Mega casting scenario with: a) continued growth, showing a shift to element surplus in the scrap with continued growth, b) the evolution with a lifespan compensated growth showing a similar shift in the supply and demand situation. |

| In the text | |

|

Fig. 10 The carbon footprint evolution from the added silicon (Si) contribution in a closed loop circular material situation for the automotive industry for the three scenarios discussed: a) continued growth of the automotive market and b) lifespan compensated growth. |

| In the text | |

Current usage metrics show cumulative count of Article Views (full-text article views including HTML views, PDF and ePub downloads, according to the available data) and Abstracts Views on Vision4Press platform.

Data correspond to usage on the plateform after 2015. The current usage metrics is available 48-96 hours after online publication and is updated daily on week days.

Initial download of the metrics may take a while.