")

")

| Issue |

Matériaux & Techniques

Volume 111, Number 2, 2023

Special Issue on ‘The role of Hydrogen in the transition to a sustainable steelmaking process’; edited by Ismael Matino and Valentina Colla

|

|

|---|---|---|

| Article Number | 201 | |

| Number of page(s) | 17 | |

| Section | Materials production and processing | |

| DOI | https://doi.org/10.1051/mattech/2023003 | |

| Published online | 14 June 2023 | |

Review

Net-Zero transition in the steel sector: beyond the simple emphasis on hydrogen, did we miss anything?☆

La transition écologique « net-zéro » de la sidérurgie : en dehors de l’attention portée à l’hydrogène, y a-t-il des questions qui demandent encore à être approfondies ? Presentée comme conference invitée à « H2 for Green Steel, 2nd International Conference », Jouy-en-Josas, 29 novembre – 1er décembre, 2022

IF STEELMAN, Semécourt, France

* e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Received:

2

January

2023

Accepted:

8

March

2023

Abstract

There is an explosion of publications and of various announcements regarding the use of hydrogen in the steel sector as a way to arrive at Net-Zero steel production − particularly in Europe. Most of them describe process technologies on the one hand and commitment to implement them quickly in the steel sector in the form of roadmaps and agendas, on the other hand. The most popular process technology is H2 Direct Reduction (H2-DR) in a shaft furnace. Available technical literature, as abundant as it may be, is still fairly incomplete in making the pathway to Net-Zero explicit and credible. This paper tries to identify important issues which are not openly discussed nor analyzed in the literature, yet. Process-wise, open questions in technical papers are: (1) what are the best-fitted iron ores for H2-DR, (2) what downstream furnace, after H2-DR, can accommodate various raw materials, (3) how and how much carbon ought to be fed into the process, (4) what is the best design for the shaft, (5) should it be designed for both natural gas and H2 operations, or simply for H2, (6) how should the progress of R&D be organized from pilot plants up to full-scale FOAK plants and then to a broad dissemination of the technology, (7) what kind of refractories should be implemented in the various new reactors being imagined, etc. Cost issues are also widely open, as a function of green hydrogen, green electricity and carbon prices. How is hydrogen fed to the steel mill and what exactly is the connection to renewable electricity? Is the infrastructure that this calls for planned in sufficiently details? What is still missing is a full value chain picture and planning from mining to steel mills, including electricity and hydrogen grids. Two years after our last review paper on hydrogen, the overall picture has changed significantly. Countries beyond Europe, including China, have come up with roadmaps and plans to become net-zero by 2050, plus or minus 10 years. However, they do not rely as much on H2 alone, as Europe seems to be doing. What is most likely is that several process routes will develop in parallel, including, beyond H2-DR, Blast Furnace ironmaking and NG Direct Reduction with CCS, electrolysis of iron ore and scrap-based production in EAFs fed with green electricity, which would single-handedly support the largest part of production by the end of the century; as more and more scrap is to become available and be actually used. There is also a question for historians. The influence of Climate Change on Steel has been discussed continuously for more than 30 years. Why has the commitment to practical answers only solidified recently?

Résumé

Il y a une explosion de publications et d’annonces de toutes sortes à propos de l’utilisation d’hydrogène pour atteindre le « net-zéro » dans la sidérurgie, en particulier en Europe. La plupart d’entre elles décrivent, d’une part, les procédés et, d’autre part, les engagements pris pour les mettre en œuvre rapidement dans le secteur de l’acier, via des feuilles de route avec échéanciers. Le procédé dont on parle le plus est la réduction directe à l’hydrogène, notée H2-DR, dans un four à lit fixe. La littérature existante, bien qu’abondante, est encore plutôt insuffisante pour rendre crédible et bien décrite les chemins techniques qui y mènent. L’article s’attache à identifier les questions importantes qui ne sont pas suffisamment discutées de façon ouverte pour l’instant. En ce qui concerne les procédés, les questions qui restent ouvertes dans la littérature sont les suivantes : (1) quelle est la nature des minerais les mieux adaptés pour le H2-DR, (2) quel type de four utiliser en aval du H2-DR en fonction du type de minerai, (3) comment et jusqu’à quel niveau ajouter du carbone au DRI ainsi produit, (4) comment redessiner le four de réduction pour prendre en compte les propriétés de l’hydrogène, (5) faut-il prévoir de fonctionner avec aussi bien du gaz naturel que de l’hydrogène ou seulement avec H2, (6) comment planifier la montée en échelle des procédés, du pilote aux unités industrielles, (7) quels réfractaires prévoir dans les réacteurs successifs de la filière hydrogène, etc. Les questions de coûts restent largement ouvertes en fonction des prix de l’hydrogène, de l’électricité verte et du carbone. Comment instaurer la liaison entre hydrogène, électricité verte el l’aciérie H2 ? Est-ce que la construction des infrastructures que cela implique est prévue et planifiée suffisamment en détails ? Ce qui manque encore c’est une vision précise et planifiée de la chaîne de valeur qui va de la mine à l’aciéire en passant par les fermes de renouvelables et les électrolyseurs d’hydrogène. Deux ans après notre précédent article de revue sur l’hydrogène, le panorama global du domaine a changé de façon significative. Des pays extra-européens comme la Chine ont publié des feuilles de route pour atteindre le net-zéro en 2050, plus ou moins environ 10 ans. Cependant, ils ne mettent pas tous leurs œufs dans le panier hydrogène, comme semble le faire l’Europe. Le plus probable est que plusieurs filières de production vont coexister en parallèle, à côté du H2-DR : le haut fourneau et la réduction directe au gaz naturel avec CSC, l’électrolyse du minerai de fer et la production en four électrique à base de ferraille. Celle-ci va d’ailleurs vers la fin du siècle assurer la fraction la plus importante de la production d’acier puisque de plus en plus de ferraille va apparaître sur le marché et qu’elle sera effectivement utilisée. Il reste une question pour les historiens. Cela fait en effet 30 ans que les conséquences du changement climatique sur la production d’acier ont été analysées. Pourquoi a-t-il fallu tout ce temps pour que la feuille de route des applications concrètes de ce travail soit lancée sérieusement ?

Key words: Net-Zero transition / steel / hydrogen / epistemic shock / addiction to fossil fuel / addiction to rare metals

Mots clés : transition net-zéro / acier / hydrogène / choc épistémique / intoxication aux énergies fossiles / intoxication aux métaux rares

Note to the reader: The article type "Original Article" was a mistake and has been corrected to "Review" on 22 September 2023.

Presented as a keynote lecture to “H2 for Green Steel, 2nd International Conference”, Jouy-en-Josas, 29 November–1 December, 2022

© SCF, 2023

“The world is going through an epistemic shock as great as the one that revolutionized Western culture between the Renaissance and the Scientific Revolution”.

Bruno Latour1, Où atterrir, comment s’orienter en politique, 2017 [1]

1 Introduction

Since the EU Commission announced its Green Deal policy in 2019, setting a target of Net-Zero for GHG emissions by 2050 and a trajectory for reaching it − an intermediate reduction in 2030 of 55% vs. 1990, there have been myriads of announcements in the European Steel community to endorse these commitments and to get organized to meet them. The Green Deal was itself a practical policy decision to enforce the 2015 COP 21 Paris commitment to keep ground atmospheric temperature increase below 1.5 or 2.0 °C in the future but also an answer to a wide demand of society to act against Climate Change − from teenagers to company shareholders. Beyond the EU, many countries followed suite with similar commitments, although some differed at the margin, thus Net-Zero by 2040, 2060 or 2070. Most of the international Steel Community also concurred rapidly.

At the start, we feel it necessary to remind the reader of some important numbers relative to Climate Change (Tab. 1). Moreover, the quote by Bruno Latour, at the top of the article, may also help put the discussion into its proper perspective.

This article focuses on hydrogen steelmaking, because it is widely seen as an important solution to enforce Net-Zero in the steel sector and is the main topic of the present conference, which is a second edition [7]. It is a follow-up on review articles written two years ago, where the thermodynamics and process engineering backgrounds were outlined [8] and the hydrogen processes placed in the wider context of competing ones and of access to green energy and green hydrogen [9]. The flurry of announcements on hydrogen has continued since, so that it is still quite difficult to review the present “state of the art” in the area, as one would wish to do it if we were given the time to develop sufficient hindsight.

The attempt is therefore to update what was reported in these previous reviews. Steel companies in Europe but also across the world have published their intentions in press releases, web pages and conference communications. Academics have published papers. We want to mention as many as we can and try to organize what has been said in order to identify what is clearly established and what remains unclear. While steel players are struggling to get things moving, they do not necessarily take the time to write down their intentions and understanding in technical and scientific terms. We will therefore try to point out what is unsaid rather than what is unknown. But some questions remain open and still unresolved.

Note that many review articles have also started to be published, while many more are in the process of reviewing by Journals [10–13].

2 State of the art of H2-DR in terms of process metallurgy

Three types of pyro-metallurgical reactors are used to reduce iron ore by hydrogen.

The most common type is a shaft reactor, i.e. a fixed-bed reactor wherein a countercurrent flow of reducing gas flows through the iron charge made of pellets. The product, H2-DRI, is extracted at the bottom of the shaft. Two major commercial processes propose solutions, derived from the background of direct reduction by natural gas, MIDREX [14] and HyL-ENERGIRON [15]. A third equipment manufacturer, PRIMETALS [16], is also active in the area with a license from MIDREX. Most of the pilot plants, demonstrators, FOAK plants under construction and simple announcements are based on either one of these technologies. They are slightly different in classical DR, but seem to differ only at the margin in the case of H2. Today, whereas MIDREX is ahead of ENERGIRON in the number of classical DR plants, H2-DR announcements seem to be in favor of ENERGIRON. Shaft-based H2-DR is the most favored process today. This is probably due to the fact that it is seen as the most mature to use hydrogen and therefore that the leap towards large scale implementation is the most credible.

Another reactor that can in principle reduce iron ore by hydrogen is a fluidized bed reactor (FB). Historically, it was tried in the laboratory [17] but also commercially for a short period of time [18], respectively in a bubbling bed and in a recirculatory reactor. The input of raw materials is powder, namely sinter feed, or more rarely, pellet feed. Direct Reduction carried out in a series of fluidized beds was implemented in the FIOR process in Venezuela, in the subsequent FINMET process, also in Venezuela and in Australia, and in the FINMET process run by POSCO in Korea: they differ by the type of reducing gas, respectively natural gas and COREX top gas. PRIMETALS was associated to both. Redesigning both families of processes to use hydrogen has been proposed under the name of HYFOR [19,20] and HYREX [21]: the first one started up a pilot plant in 2021 at Donawitz’ voestalpine steel mill, and the second is in the design stage at POSCO, in Korea. Academic studies have also come out [22]. These are recent significant advances of the technology, although fluidized bed hydrogen reduction is still less developed in terms of TRL and of number of plants than shaft DR.

The third type of reactor for hydrogen reduction of iron ore is the flash smelting reactor [23], that may use a hydrogen plasma torch [24]. The principle is to carry out the reduction of powdered iron ore, preferably pellet feed, at high temperature inflight, thus very rapidly. Both US (FIT) and European projects (PRIMETALS on the premises of voestalpine at Donawitz’ steel mill) are carried out at laboratory or pilot scale. Flash Smelting hydrogen reduction is thus presently less developed in terms of TRL and of number of plants than both FB and shaft DR.

In what follows, the focus will be mostly on shaft reduction, based on the guess that this technology will dominate H2-DR in the near future.

3 Raw materials

A DR shaft furnace operated with natural gas is fed with so-called DR pellets, usually prepared by the iron miner. They are distinct from blast furnace (BF) pellets, prepared either by the miner or by the steel producer. Both types of pellets are available commercially and the supply is directly related to their relative demand [25]. Moreover, iron ore is also available as lump ore and powdered, particulate or pulverized ore, most of which is sinter feed meant for sintering strands that amount to 60% of iron needs for the present blast furnaces.

Table 2 shows the main properties of these pellets.

DR pellets, typically, have an iron content of more than 67% Fe, small acid and basic gangue contents and low concentrations in P and S. They are the “gold” of the iron ore supply.

The assumption today is that H2-DR will call on DR-grade pellet. Therefore, the transition to H2-reduction will increase the demand for DR-grade pellets as blast furnaces get shut down and the question arises of whether enough quantities will be available. In terms of overall quantity of iron ore, there is no risk of scarcity, even taking on board a significant increase in future steel production, but there are worries about ore quality to produce much larger quantities of DR-quality pellets.

Based on the present situation, a number of steel producers, in Europe in particular, have posited, more or less implicitly, that DR pellets would not be available and therefore that BF pellets should be used. This has important consequences in terms of what furnace can be used to melt the DRI, as it would contain more gangue and possibly also more phosphorous and sulfur.

Today, iron ore mining and steelmaking operate in silos, as far as strategy and foresight are concerned, and discussions on iron ore demand for the hydrogen transition in steelmaking and of supply have not yet arrived in steel-focused conferences. The issue is starting to be addressed by experts in the field [27–29], but much more will be needed in the future to arrive at a deeper understanding of where one might arrive, collectively, when the Steel transition is properly taken on board by the mining sector. Each protagonist has to convince the other that a major paradigm shift is under way, which will require a deep strategic remodeling of iron ore mining. Increase in pelletizing capacity delivering DR quality in existing and new plants, more ore beneficiation to upgrade the mining output from BF to DR quality, search for and start of operation of higher quality iron deposits, etc. There have been announcements, like the conversion of AMMC’s pellet plant in Port Cartier to upgrade 100% of its 10 Mt pellet capacity to DR-grade, and more. But what would probably be needed now is an overarching strategic roadmap for mining and steel to advance together towards Net-Zero in their shared value chain. Incidentally, the Mining sector should also disclose its Net-Zero transition plan in details, like LKAB did in Sweden [30].

4 What kind of melter follows the H2-DR shaft, an EAF, an OSBF, an SAF or something else?

Downstream of the hydrogen reduction reactor, a second reactor is needed to melt the DRI and convert it further down the steel value chain. For obvious reasons, this reactor ought to be some kind of electric furnace, fed with green or blue electricity.

A “simple” Electric Arc Furnace (EAF), initially designed to melt steel scrap, can only accommodate small amounts of slag (about 120 kgslag/tsteel): on the other hand, it directly produces liquid steel. It can also melt DRI, up to 100%, in which case it would generate roughly up to 360 kgslag/tsteel. An EAF is tapped through a snout by titling the furnace, unless it is equipped with an EBT (Eccentric Bottom Tapping) . H2-DRI generated from DR-grade pellets could be melted in an EAF and would thus be an exact transposition of the NG reduction flowsheet. This H2-DR route qualifies as a kind of minimill.

Many H2-DR demonstrators or FOAK plants follow that scheme, in particular HYBRIT which uses high-quality pellets made of LKAB’s magnetite2. So does the SALCOS process line or the Chinese HBIS line.

Using lesser quality ore in the form of BF pellets would bring more gangue into the furnace (up to twice as much) and therefore proportionally more slag. This could not be accommodated by an EAF and this is the reason why electric furnaces of the kind that accepts large amounts of gangue/slag become necessary. They are commonly used in the production of ferroalloys, namely the Submerged Arc Furnace (SAF) or variants that have been imagined, like the Open Slag Bath Furnace (OSBF) proposed by Tenova in an iBLUE process line [15,31,32], or the Open Slag Bath Smelting Furnace (OSBSF) of Metso Outotec [33], or other reactors like the Electric Smelting Furnace (ESF) of POSCO (which is rectangular rather than circular and works with 6 electrodes) or furnaces simply called melter or smelter. These furnaces simulate a Blast Furnace, except that their energy stems from electricity and no longer from carbon. Like a BF, they also generate hot metal rather than steel: they were actually designed to carry out significant reduction beyond simply melting DRI, even of mediocre quality. The heating mechanism is either through conduction heating in the slag (SAF) or from the radiation of an electric arc (OSBF, OSBSF), like an EAF does. The electrodes are of the Soderberg type, rather than purchased graphite electrodes. The furnace is tapped from the side, with separate tap holes for slag and hot metal.

Note, however, that even though some limited pilot experiments were carried out by Tenova [34], there are no industrial references yet of using that technology in connection with an H2-DR shaft.

Many H2-DR demonstrators or FOAK plants propose to use such a furnace, even if the announcements do not name it explicitly: TKS in Dortmund [35,36], ArcelorMittal in Dunkirk [37], Tata Steel in IJmuiden [38],

Such a scheme makes it necessary to send the hot metal to a converter and further on to ladle metallurgy, continuous casting3 and so on. This, in effect, adds an extra process step compared to the DR-EAF route and probably increases operating costs, although some of them may be compensated by the lower price of BF pellets vs. DR pellets. Due to the similarity to the traditional Integrated Steel Mill route, steel producers feel confident that they can produce the same high-end products that they have been providing to their customers, especially in flat products. There might be less cuts in the workforce. Note, however, that this route introduces carbon (4.5% in the hot metal), which ends up in the atmosphere as CO2: the route, therefore, does not reach Net-Zero! The iBLUE solution, however, takes this matter on board by capturing these emissions and handling them via CCUS – for the time being in a conceptual manner.

Note also that the DR-OSBF route generates slag “like” a blast furnace does and, as such, can continue to deliver it as a raw material for the cement industry, which helps it cut its GHG emissions [39]. In a perfect world, the reduction in emissions of both the steel and cement routes should be taken on board together, especially in terms of carbon value [40].

5 How to handle the endothermic reactions?

Contrary to reduction by CO, which is mostly exothermic, all the H2 reduction chemical reactions are endothermic and therefore require external heat to be introduced into the process. In a process model, this can be done by a sleigh of the hand, but actual engineering solutions need to be implemented into the process design.

The topic, although acknowledged by process designers, is not openly discussed in details. The use of electrical heating is possible, as is the preheating of hydrogen prior to entering the shaft, by recovering process heat, burning hydrogen as a fuel or introducing some natural gas in the loop. All of this is facilitated by the fact that the reducing gas potential is not exhausted at the top of the furnace and therefore has to be recycled back at the bottom, like it does in NG reduction.

6 Optimization of shaft size to match the reducing power of H2

The major feature of H2-DR shaft furnaces as they are represented in the literature today is that they look more or less exactly like natural gas shafts in terms of height and diameter. The reducing power of hydrogen, however, is higher than that of CO and, intuitively, this should translate into a more compact reactor.

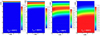

Figure 1 represents a shaft furnace designed in height and diameter to operate with natural gas, but the simulations refer to H2 operation.

The simulations show that, if the furnace is operated at an injection temperature of pure hydrogen of 800 °C, then the reduction reactions take place entirely in the top part of the reactor: the bottom of the shaft is mostly useless. A reactor custom designed for operation under pure hydrogen should, therefore, be quite different from the classical MIDREX or ENERGIRON shafts and maybe as much as half of its height, although this would need to be refined very carefully. Another option would consist in increasing the throughput of the reactor. In natural gas (NG) reduction, the bottom of the shaft is needed to reach a metallization degree of 95%.

Now, is it relevant to imagine that such a shaft would always be operated under pure hydrogen? Or should provisions be made for a back-up plan to operate also with natural gas? Or would such a NG operation be a bridging solution, before pure hydrogen is readily available from a grid? This seems to be an implicit assumption in today’s literature for several reasons: (1) as an intermediary solution to ramp up slowly to Net-Zero and meet an intermediary target in emissions in 20304 or (2) have NG as a backup if the hydrogen supply is disrupted, or (3) other arguments for starting up or shuttering down the shaft under NG.

Whether the H2-DR shaft should be a hybrid shaft, allowing for NG operation as well, thus remains an open question in the present discussions shown in the literature.

Note that the recent announcement of SSAB to move more quickly to the hydrogen transition than initially planned might mean that pure hydrogen operation is easier than imagined, after the extensive investigation that they carried out on their HYBRIT demonstrator and the provision they made to secure a steady in-flow of hydrogen by incorporating a buffer hydrogen storage facility in their plant design.

|

Fig. 1 REACTOR simulations of a shaft furnace under pure hydrogen, showing the regions where Fe2O3, Fe3O4, FeO and metallic iron are present, when the gas is injected at 800 °C. The charge is hematite pellets. The representation is axi-symmetrical, with the reactor axis shown to the left [8]. |

7 Other open issues

Another important issue is the matter of the carbon content in H2-DRI.

The question does not arise in the DR-OSBF route, as it goes through a hot metal step.

In the H2-DR-EAF route, however, this is a legitimate interrogation. Tradition in the classical production of DRI is to provide some carbon in the DRI, typically 1 to 4.5% [41]. This was meant both to ease up the discharge of DRI from the shaft and to facilitate EAF operation, at a time when introducing fossil energy in the furnace, through the so-called “oxygen injection”, was a legitimate and economically reasonable pursuit. This can also be done in the case of H2-DR, by introducing some NG into the shaft – thus reverting to an operation similar to HyL and making reaching Net-Zero more difficult. Carbon can be introduced in the form of charcoal in the EAF, which, if it qualifies for carbon neutrality, would avoid this difficulty.

Note also that an important feature of H2-DRI is that it can be carbon-free at the exit of the shaft and this goes along with a higher degree of metallization than NG DR5.

Obviously, the rationale for choosing how much carbon will be needed, how it should be introduced and how it can be compensated to get closer to Net-Zero is still evading clear public debate.

A further open issue that will be mentioned here is that of the refractories used in H2-DR. In a reducing atmosphere like high-temperature H2, it is well known that iron-bearing refractories should be avoided. The literature on the subject is slowly being fleshed out [42–46], including in the present conference [47,48], but we have not yet identified an overarching review nor practical presentations of what operators of pilots or demonstrators are using. Some of these references refer to the use of hydrogen as a fuel in a (re)heating furnace rather than as a reducing agent in a metallurgical reduction reactor.

8 Integration with green hydrogen and electricity

Process engineering related to H2-DR is fine, but it only covers scope I GHG emissions. In order to achieve Net-Zero, green or any other carbon-free hydrogen is also necessary to ensure low scope II emissions.

Announcements of capacity increase of electrolyzers have been accelerating with more than 200 MW of capacity entering operation in 2021 to reach 0.5 GW. It is expected to double by the end of 2022 and to grow to over 1 GW by the end of 2022 [49]. Announced investments could lead to an installed electrolyzer capacity of 134–240 GW by 2030. The manufacturing capacity of electrolyzers should be on track with these projections (construction of “mega-factories”). This growth, however, is still too slow, according to the IEA, to reach 700 GW by 2030 and thus to be in line with a Net-Zero emission scenario by 2050.

There are several technologies to generate green hydrogen by electrolysis of water or steam and a number of non-electrolysis processes (production from “proper” (carbon-neutral) biomass, reforming of natural gas with CCUS, etc.), see recent reviews in [50,51]. Electrolyzer technologies rely on high-temperature Alkaline Water Electrolysis (AWE) or derive straightforwardly from those of hydrogen fuel-cells and the two relevant ones are PEM (Proton Electrolyte Membrane) and SOEC6 devices. A detailed description is out of scope for this review. Let us say simply that PEM is state of the art and that giga-factories are being built by several industrial outfits across the world to produce cell stacks [52–54]7. These are “general-purpose” electrolyzers meant for transport as well as industrial applications in the short term. The SOEC electrolyzers work at higher temperatures (500 to 850°C) and thus convert steam rather than water into hydrogen. They are still under development, although a large device has been developed by Sunfire in the framework of a project called GrInHy2.0, run by Salzgitter in Germany as part of its SALCOS program [55]; its power input is 720 kW. They are more energy efficient than PEM electrolyzers (94% electrical efficiency vs. 60% for PEME), but, as they need to stay at temperature for long periods of time, they are imagined as contributing mostly to industrial uses of hydrogen. Thus, schematically, one may project that AWE and PEM electrolyzers will be used in the H2-DR plants erected in the short term and SOEC later in time.

Green power supply is the responsibility of electricity facilities, from the standpoint of most steel producers. It is up to them to deliver the proper amount of power to the electrolyzers, which will then feed the steel mills. However, this is a somewhat theoretical viewpoint, as green power, hydrogen and steel consumption will need to be coordinated at the level of capacity investment and of the flow of the various fluids in real time. This is only described in very general, macroeconomic terms, for example in the IEA power roadmap [56] and in various similar national documents, but they do not clearly connect with the detailed, site by site needs of the steel sector. Moreover, it would be nice to explain how the interfaces between power and hydrogen and hydrogen and steel mills will be run and maintained in tension. Some steel producers have signed agreements with electricity facilities to supply them with green power, as analyzed in details in [57]. The modalities of transport and the amount and nature of the buffers will need to be analyzed and built, eventually. Moreover, the need for raw materials to feed the steel mill will also require this coordination to include the mining sector.

In the background of these issues lie the matter of the localization of hydrogen generation and of steel production. It seems to be taken for granted, from the steel operators’ standpoint, that the steel mills will stay where they presently are. It is also taken for granted that hydrogen will be generated close to the consuming steel mills. This is probably too quick an analysis, however. Indeed, hydrogen can be generated close to the energy production region and shipped far away, by ship or pipe, as hydrogen or as ammonia: the case for producing hydrogen in the Middle East, from gas by methane reforming and storage of CO2 in local underground pore space or for Enhanced Oil Recovery (EOR) is made in [58]. Another option would be to produce DRI from hydrogen at or close to the iron ore mine, as discussed in [59]. Several Mining companies are actually considering moving their business downstream and to sell DRI rather than pellet feed or even pellets to their customers. Thus, LKAB has announced that it would market 5.4 Mt of DRI per year by 2030 and 24,2 Mt by 2050 [60].

A map of hydrogen logistics remains to be built. A study by Deloitte is shown in Figure 2, as an example.

|

Fig. 2 Projected European hydrogen backbone in 2040 (courtesy of Deloitte). |

9 Roadmap targets

The targets of the EU Commission Green Deal guarantee to reach ≤1.5 °C in 2050, if they are applied universally, i.e. beyond steel, and internationally, i.e. beyond the EU.

Aiming at the 2050 targets, but missing the 2030 one will compromise the final temperature reached. Thus, it is fine to announce Net-Zero by 2040 or even earlier, but less than 55% reduction by 2030 (cf. the FF55 package [61]), or Net-Zero by 2060 or 2070 are not so fine! Moreover, it is not clear how the ambitious commitments of neutrality by 2050 compensate for 2030 intermediate targets that fall short of 55%.

Note, incidentally, that the various roadmaps refer for 2030 to targets measured against many different years, the industrial revolution (1850), or 1990 (like the EU Green Deal does), or the present or some other date. They also refer to earlier version of EU targets. This does not help the reader, as a conversion rule between the various metrics is not readily available, so that one is left with the impression that the fuzziness of the statements is left on purpose.

Furthermore, there are still gaps to Net-Zero in terms of technology proposals. How to close them? By compensating emissions? Or by introducing negative emission processes [62] including atmospheric carbon capture [4], assuming that it is possible at a significant level?

Targets should be life-cycle targets or scope I, II and III: all of society ought to align with net-zero targets by 2050, which is a delicate mechanism to set up. When this is done, the good news is that we will not have to worry about scope I, II or III emissions any more, as all will be nil! We will just have to make sure that emissions are not allowed to increase again afterwards.

10 National and industry Net-Zero steel roadmaps

Global world steel roadmaps were published in large numbers for the last 20 years. We only mention the earlier and the later ones [63–68]. They are quite close, reworking similar assumptions again and again, but rarely acknowledging the previous work. Their message is that net-zero and, therefore, the commensurable contribution of the steel sector to the 1.5 °C Paris target are possible. Hence the name of the “Mission Possible” last mentioned report. It was then up to the individual steel companies to roll out their own plan to achieve that target and to fit it inside this general plan.

Today, virtually all the steel companies in the world have complied, which goes significantly further than what was available when the previous paper what written in 2020 [9]. The information has been published in press releases in communication style and, therefore, it is sometimes unclear, technically.

ArcelorMittal, which operates the largest number of steel mills in Europe, has Net-Zero plans for all of its major sites, in Germany, Belgium, France and Spain but also beyond: the transition pathway is shown in Figure 3 [69,70]. Its plans are to become Net-Zero in 2050 and to cut emissions in 2030 by 35% in Europe and 25% in the world compared to today’s. In Dunkirk, plans comprise switching in part from ore to scrap, thus implementing EAFs, shutting down blast furnaces, replacing them with H2-DR from MIDREX, and combining DRI and scrap feed; moreover, a blast furnace should remain in operation with CO2 capture and storage planned in the deep saline aquifers of the Northern Lights site in Norway [71]. Fos should shut down its 2 BFs and replace them by a scrap-based EAF. In Spain an H2-DR shaft will produce HBI in Avilès to be melted in the Sestao mini-mill. In Belgium, two H2-DR shafts are planned in Ghent and the BFs ought to be shut down. Same storyline for Bremen and Eisenhüttenstadt mills8, while Hamburg should host the first H2-DR shaft of the group to serve as a demonstrator and build experience on the technology (agreement with MIDREX signed in 2019 and industrial maturity expected by 2025).

In Canada, ArcelorMittal Dofasco in Hamilton will install a H2-DR shaft from Tenova (ENERGIRON) [72].

Thyssen Krupp Steel (TKS) operates one major steel mill in Duisburg, presently with 3 blast furnaces. A step-by-step conversion to H2-DR is planned with a smelting electric furnace producing hot metal and then delivering it to the existing BOFs [36].

Tata Steel operates one steel mill in IJmuiden, with presently 2 blast furnaces. A Direct Reduced Iron Plant (DRP) and a Reducing Electrical Furnace (REF) will replace them, a decision announced in September 2021 [73].

Salzgitter A.G., the second largest German steel producer, has been engaged the longest in Germany in planning its Net-Zero transition, by developing the SALCOS program [74]. The plan is to phase out the two BFs and to replace them, stepwise, by three “DRP-EAF” plants to reach 82–95% GHG reduction by 2050. Note that Salzgitter has been preparing the transition through several research programs that include the development of a high-temperature, solid-oxide steam electrolyzer called GrInHy2.0 [75].

SHS (Stahl Holding Saar) has committed to carbon neutrality by 2050, based on the use of hydrogen, but only the first step, injection of coke oven gas and then of pure green hydrogen produced in Lorraine, France and in Saar by photovoltaics, has been explicitly described [76].

Voestalpine of Austria has also been engaged for a long time in its low carbon transition, via a series of EU research projects [77]. H2FUTURE is experimenting a large 6 MW water electrolyzer in Linz [78]. The SuSteel (Sustainable Steel) project, based on a hydrogen plasma furnace (see before) is being developed at a pilot facility in Donawitz with PRIMETALS. The company says that it plans to assemble these elements to become carbon neutral by 2050.

SSAB of Sweden has been engaged in the development of shaft H2-DR through its HYBRIT project, a large program encompassing the sintering of pellets using bio-oil, a full-scale pellet production unit in Malmberget, a facility for buffer storage of hydrogen (100 m3 at 250 bars), an H2-DR demonstrator built by Tenova in Luleå, and an EAF for melting the DRI to be built at scale in Oxelösund [79]. Note that the project is run jointly with LKAB, the mining company, and Vattenfall, the electricity facility. Commercial delivery of HYBRIT steel is planned for 2026. Moreover, the company has recently (2022) announced that it would move its target of carbon neutrality 15 years ahead of the one announced previously, i.e. to 2035. Plans are to shut down the 3 BFs in Luleå and Raahe and to replace them directly with H2-DR-EAF production, without using natural gas as an intermediary step. They make provisions, though, to feed the EAFs with both H2-DRI and steel scrap. SSAB’s plans are the most mature in the world, planned to be deployed in the fastest calendar: this is due to the direct access to LKAB high quality ore fit for DR-level pellet production and to the extensive research and development program that was started early, going through the necessary steps of scaling pilots up at the proper pace.

More companies in Europe and North America have outlined Net-Zero commitments, but they will not be reviewed further here [80,81].

Note that every company involved as well as steel business organizations stress the high level of investment that the transition will require, along with higher operating costs. A discussion was proposed in [9], where two main points were made: costs, both CAPEX and OPEX, are bound to decrease along a learning curve, like what is already obvious for the price of green electricity or of lithium-ion batteries, but this is unlikely to bring the costs of H2-DR technologies below those of conventional steelmaking and an extra price of carbon will have to be taken on board to pay for that remaining gap. EUROFER has estimated the cost of the transition of the steel sector in Europe to at least 13,8 G€/year from now until 2030 and to 8,4 G€/year until 2050, which altogether would correspond to a CO2 price of 97 €/t in 2030 and to a global cost of 280 G€ [82]. More papers are starting to cover these points [83]. Of course, none of these figures can be taken for granted as they stand, yet.

For the time being, the costs of the research steps are partially covered by EU and national fundings, and the demonstrators or FOAK plants subsidized by national government or by the EU in Europe. Steel companies, of course, also contribute. The overall financing picture is not fully clear, however.

The most recent piece of information regarding H2-DR, which has come up since 2020, is that Asia has joined the European bandwagon and started to publish national and company roadmaps.

Japan, which has been active on this topic for more than 20 years through the COURSE50 program [84], developed a national roadmap that targets Net-Zero for 2050 [85,86] (Fig. 4). The plan is to continue energy saving targets until 2040 and to implement breakthrough technologies between 2040 and 2050. Nippon Steel and JFE have their own roadmaps, which are more explicit.

Nippon Steel plans to cut emissions by 30% in 2030 vs 2013 by implementing the COURSE50 BF technologies (injection of in-house H2) in all of their existing BFs; then it will move up to SUPERCOURSE50, where H2 will be sourced from outside green energy, an H2-DR process will also be developed (shaft? Aiming both at high- and low-quality iron ore), while a new process for a “large size, high-grade” EAF production, based on the experience of the Hirohata furnace, will be developed; the DRI will be fed both to the BF and to the EAF.

JFE plans to transform their BF into a top gas recycling version with CCUS (in particular, production of methanol) and thus to cut its emissions by 50%, to design and implement an H2-DR process coupled to an EAF, the route being fed from low quality iron ore, and to build a large, high-efficiency EAF to melt DRI and scrap and to provide refining functions: JFE will implement the proper linear combinations of these processes which would make Net-Zero possible. Note that, in Japan, they insist explicitly on the need for “external conditions” to be met: a willingness of customers to purchase green steel (implicitly at a higher price), the availability of green electricity and of green hydrogen and of public infrastructures for CCS.

In China, two companies, Baowu and HBIS, have shared their plans for Net-Zero internationally, which is both new and essential, given that the country produces more than half of the world steel production today.

Baowu’s (上海宝钢集团) roadmap is based on several process concepts, which they call HyCROF for “Hydrogen-enriched, Carbon dioxide Recycling Oxygen Furnace” [87] (Fig. 5):

a sintering process using microwaves to heat up the charge and hydrogen to carry out some pre-reduction (zero-carbon agglomeration);

a blast furnace with top gas recycling, separation of CO2 and reinjection of the carbon monoxide enriched in hydrogen at two levels of tuyeres, with pure oxygen introduction rather than air and biocarbon injection;

CO2 is either stored underground or used to produce chemicals;

the program has a chapter on producing high grade steels through a near-net shape casting technology.

A demonstrator went on stream on 2 August, 2022 and has already demonstrated a 25–30% reduction in emissions, without CCUS.

Baowu had also plans for an H2-DR shaft FOAK plant with a capacity of 1 million tons per year built by Tenova Danieli in Zanjiang, China. It will use coke oven gas, natural gas and pure hydrogen and is meant to ramp up to 100% hydrogen. The process seems to have some particular features, but they are not described in enough details to be reported here. The startup is planned for early 2024 [88].

HBIS (HeBei Iron & Steel, 河钢集团) is the other Chinese company with a low emission roadmap: the target is carbon neutrality in 2050 [89]. An H2-DR shaft from Tenova was launched on 10 May 2021, to start up in Zhang Jiakou, Hebei. It will utilize a gas mix of 30% coke oven gas and 70% hydrogen from external sources.

India, the other economic powerhouse in the Far East, has a strong steel sector which is expected to grow threefold by 2050: a national roadmap was published in 2022 [90]. It takes on board all the technologies investigated elsewhere in the world, including hydrogen, as potential solutions for India and targets Net-Zero for 2070.

To stress the complementarity of the various Net-Zero processes, we have proposed a simple model of how they will cohabit and thus cooperate together (Fig. 6) [91]. Today (2020), steel production, worldwide, is distributed among blast furnace, EAF (noted as scrap on the figure), and direct reduction with natural gas. The scrap resource will increase to reach 70% of market share by 2100 (green line) and will be used entirely. The other processes will deliver the complementary steel. By 2050, the remaining BFs will be equipped with CCS and so will DR plants based on NG. In-between hydrogen and electrolysis of iron ore, assumed to grow at the same pace (the two lines are almost superposed), will replace the BF until it becomes carbon neutral in 2050.

|

Fig. 3 Transition pathway of ArcelorMittal’s steel mills (world perimeter) towards Net-Zero [69] (courtesy of ArcelorMittal). |

|

Fig. 4 The Japanese Carbon Neutral plan for the steel industry (source: METI). |

|

Fig. 5 Baowu’s Carbon Neutral metallurgical technology roadmap. |

|

Fig. 6 Model projection of the market shares of various steel production processes in the world in the 21st century. The curves for hydrogen and electrolysis are overlapping. Scrap means EAF production based on scrap. |

11 Carbon offsets/credits, negative emission processes

Net-Zero in its rigorous formulation of full carbon neutrality is difficult to achieve, as it would require each step in the process chain to be Net-Zero. However, there is a series of solutions to alleviate this difficulty.

“To achieve net-zero emissions by 2050, we anticipate any gaps remaining from the above processes can potentially be closed through the use of carbon offsets or credits. Offsets and credits are a last resort, and our preference would be to lower emissions as much as possible through technological means before purchasing offsets and credits”, says USS [80]

Another solution would be to capture CO2 from the atmosphere and send it to storage via CCS (or CCUS?) in making sure that this can be done efficiently, therefore witout any open venting of fumes, etc.

12 Further open issues

This paper has been reviewing published information related to steel, but there are other relevant topics that were left aside. First of all, there are plans to use hydrogen in other industrial sectors. Moreover, hydrogen has also become a hot topic in the investment world. Finally, the approach we have followed is strictly STEM: a broader one, based on SSH, would yield a wealth of other interesting viewpoints.

In order to reach Net-Zero, hydrogen has been called upon by many energy-intensive industries, i.e. by those which are also loosely called “hard-to-abate” sectors9 today. Thus, the chemical sector, which already uses hydrogen to produce ammonia, one of its major large-scale products needed to make fertilizers and methanol, and in its refining sector to hydrocrack heavy oil, is planning to switch to green and blue hydrogen and to use more of it, in combination with CO2 to generated sustainable feedstock – as a source of heat to replace natural gas and to generate sustainable fuel for transport (hydrogen trucks, ships, trains) [92]. The non-ferrous metals [93] and cement [94,95] industries have also published roadmaps implementing hydrogen as a reducing agent or as a fuel. The transport sector, heavy-duty road vehicles, ships, possibly airplanes, will also probably call on hydrogen in the future.

Also, there remains a question for Historians. Why have we collectively been slow in the steel sector (and beyond) to tackle Net-Zero solutions, while the matter was quite well recognized and solutions had been worked out at a reasonable level of TRL, many years ago [90]?

13 Conclusions

The explosion of announcements, but also of genuine activity in the steel sector to achieve Net-Zero by the middle of the century is quite impressive.

This is clearly related to the COP21 “Paris agreement” of 2015 but also to its implementation as a regional policy in the European Union under the name of the European Green Deal (2019). Within months, business communicated that they supported this move and developed their plans to implement it in their operations. Outside of the EU, many countries and businesses followed suit with their own version of the Green Deal.

The review presented here covers the steel sector. It is a press review rather than a literature review, given the nature of the sources, which do not all qualify as peer-reviewed scientific articles.

An important question is whether the announcements made by a business constitute a simple communication exercise or a commitment. Of course, we cannot answer that in a clear and unambiguous way. But the press releases are first communication exercises and and some of them may eventually amount to greenwashing.

Now, what is new compared to 2 years or to 20 years ago? Two years ago, the explosion of announcements and the enthusiasm for hydrogen in particular was already obvious. Since then, however, the announcements have been fleshed out in Europe by countless seminars and conferences ripe with specific roadmaps and by plans to erect pilots, demonstrators or even FOAK plants. Furthermore, roadmaps were published from all over the world and have started to be implemented in a manner similar to what is happening in the EU. Twenty years ago, the literature was already rich but originated mainly from researchers, both from academia and industry. Moreover, while there is a general consensus today to abide by the terms of the Green Deal, with the caveats mentioned in the text, work done 20 years ago did not mention Net-Zero but only reduced emissions, for example 50% reduction vs. 1990 in the case of the ULCOS program10.

Hydrogen is mentioned in roadmaps from all over the world, although the EU focuses more on this solution that the Far East. Moreover, in Europe, hydrogen is more single-mindedly selected by companies, which operate one (or two) steel mills. The commitments made by member states [96,97] and the EU [98] to subsidize hydrogen, have also probably played a role in creating that enthusiasm.

Thus, the steel sector will probably not overwhelmingly shut down its blast furnaces and replace them by hydrogen direct reduction plants. BFs are likely to remain operating in Europe, in the big companies which operate a large number of steel mills, like ArcelorMittal. In Asia, where companies also operate several integrated steel mills, they will also keep BFs operating. They will all exhibit some kind of carbon capture technology and further storage or utilization (CCUS). Moreover, other solutions, like using more scrap locally and carrying out the electrolysis of iron ore should also be considered among the likely futures. All likely solutions are brought together, for example, in [9,90].

Among hydrogen direct reduction technologies, the shaft furnace seems to be preferred, either based on ENERGIRON or MIDREX schemes. Fluidized beds are the solution planned in Korea by POSCO (HYREX) and PRIMETALS also advertises the HYFOR process. Hydrogen Flash Smelting technology is explored at pilot scale in Austria (SuSTEEL) and in the US (FIT process). Shaft reduction is more advanced in terms of planned units. But both competing technologies are likely to be pursued with determination.

There remains a large gap to bridge in order to switch to hydrogen reduction, even in a partial way.

What is needed is a full value-chain approach, from raw materials extraction and green energy generation all the way to the production of steel. The steel sector has been concentrating on process technology and treating only conceptually what lies outside of its business boundaries: thus, the future availability of “good” DR-grade pellets vs. “bad” BF-grade pellets is still an open issue so that the exact succession of processes in the future H2-DR steel mill is still a matter of conjecture. Similarly, how hydrogen generation by water (or steam) electrolysis can be ramped up to feed the steel sector’s needs and how it will connect with green electricity to be erected from scratch is not planned in details: open questions are the geographical location of the REN farms, of H2 generation plants, of steelmills, the distance between users, the structure of green electricity grids, of green hydrogen grids, of overseas transport, etc. still need to be planned in details. Notice that some steel operators are taking on their shoulders the responsibility of generating hydrogen. But most of them rely on “external conditions” to align with the needs of steel: that would call on an overarching, coordinated planning of investments across the value chain, which is not openly discussed yet11. The need is urgent and problematic, to get all these stars aligned – from mining, to more green electricity generation, to hydrogen mass production, to a hydrogen grid creation, to H2 use by steel (and other activities), etc.

Also missing is a structured discussion of the transition pathways from today’s steel mills to the Net-Zero mills of the future. An underlying question is how much pilot work is necessary before an industrial investment can be safely announced? Moreover, even if an H2-DR steel mill was erected soon, it would rely on hydrogen and electricity which are not yet Net-Zero: it could not claim to be net-zero before its upstream value chain were itself net-zero. This is an important part of the transition pathways. Last, emissions from the steel mill downstream of primary production ought to be transformed to net-zero technologies: these are being openly discussed in fair details but the concatenation of a whole mill from raw materials too steel is still to be described and its implementation planned.

One of the obvious conclusions of this review is that H2-DR is quite complex to set up as an industrial process, more than it may have seemed at the outset, when most observers imagined that a simple H2-DR-EAF route would suffice. It might therefore be worthwhile to reconsider the choice of H2-DR and to reevaluate a BF with CCS instead. The decarbonization of the blast furnace is simple enough by itself: what is more complex is the need to set up a CCS network and to finance it. But is this more complex than setting up a much-enlarged green electricity network, an electrolyzing industry and a hydrogen grid? Since conditions seem to have changed, this should probably be investigated again more closely. Notice that this solution remains a strong component of the carbon neutral futures in the Far East.

At the end of the day, hydrogen remains a magic word: some would say that it has agency [99], other that it is a dream… It is, anyway, in line with the messianic book of Jeremy Rifkin, the Hydrogen Economy (2012), which foresaw a huge future for hydrogen but, at the same time, sold unphysical ideas about the element! Hydrogen is still considered as a kind of Swiss knife, that can solve several difficult issues at the same time: that of the so-called hard-to-abate industries, of the transport of heavy loads on land, on water or in the sky and of the replacement of natural gas as a gaseous fuel. This probably explains why governments have been seduced by it and have encouraged it. Beware, however, that we collectively do not cure an addiction to fossil fuels by an addiction to scarce metals!

Paraphrasing Bruno Latour, who spoke of an epistemic shock, one may say that the world is experiencing a major geopolitical paradigm shift, from a world addicted to fossil fuels to one addicted to specific, rare, expensive and carbon-heavy metals. Obviously, quite a challenge!

If we collectively meet the Green Deal targets by 2050, then the post-2050 constraints will change radically. Of course, the measures taken to reach that point will have to continue unabated: for example, the collection of steel scrap will have to be maintained at the highest possible level and so on. Of course, it will have been necessary to arrive at that point by taking on board an Environmental Return On Investment (EROI). By then other environmental threats can come to the forth and concentrate efforts of the steel sector, for example emissions, especially to air, which are related to large numbers of premature deaths according to WHO12 [100–102], measures to slow down the collapse of biodiversity and so on.

In the longer term, peak population will presumably take place, which ought to be followed by a peak steel13, if we assume that steel production and population levels are correlated. This should take place towards the end of the century or early in the next one. By then, most of the present efforts to reach Net-Zero will have become obsolete and whatever ironmaking furnaces remain by then will have to be shut down for good. Steel will by then have entered a fully circular economy14.

If, somehow, we do not manage to reach the Green Deal targets, then the future will be quite different from what is commonly discussed in scientific papers and in political agendas. Temperature increase will overshoot 2C. This is the field of collapsology [103,104], an academic discipline, and of fiction, which explores these futures in the framework of post-apocalyptic or other science fiction stories [105].

The present paper is definitely on the side of STEM disciplines, thus based mainly on the contributions of engineers. SSH disciplines, however, would probably have much to say on the topic, although this line of thinking has not yet entered into conferences and papers meant for engineers and business people. Humanities and in particular literary criticism have already closed that gap, though, when they discuss environmental issues, see for example [106]. History as well is developing a new research field devoted to the history of climate change [107]. It is being lively pursued by on-going research [108], but also follows more popular works published by Jared Diamond [109].

Acronyms

AWE: Alkaline Water Electrolysis

BOF: Basic Oxygen Furnace

BF: Blast Furnace

CAPEX: Capital Expenditures

CCUS: Carbon Capture, Utilization and Storage

CCS: Carbon Capture and Storage

COP21: 21st Conference of the Parties of the UNFCC, held in Paris in 2015

COURSE50: CO2 Ultimate Reduction System for Cool Earth 50, the name of a National Japanese research and development program

DOFASCO: A steel Mill of ArcelorMittal in Canada, bearing the name of the former company Dominion Foundries and Steel Company

DR: Direct Reduction (of iron ore)

DRI: Direct Reduced Iron

EAF: Electric Arc Furnace

ENERGIRON: Process name by TENOVA, designating the HyL direct reduction process

EOR: Enhanced Oil Recovery

EROI: Environmental Return on Investment

EU: European Union

FF55: Fit for 55, an EU policy targeting 55% reduction in GHG emissions vs. 1990

FIT: Novel Flash Ironmaking Technology (University of Utah)

FOAK: First Of A Kind (steel plant)

GHG: GreenHouse Gases

GrInHy2.0: Green Industrial Hydrogen, a research program of Salzgitter connected to SALCOS

H2-DR: Hydrogen Direct Reduction

H2-DR-SAF: route composed of an H2-DR and an SAF

H2-DR-EAF: route composed of an H2-DR and an EAF

HBIS: HeBei Iron & Steel, 河钢集团, China

HYBRIT: Hydrogen Breakthrough Ironmaking Technology, Sweden

HyCROF: Hydrogen-enriched, Carbon dioxide Recycling Oxygen Furnace, China

HYREX: a direct reduction process based on hydrogen derived from FINEX, Korea

HYFOR: HYdrogen-based Fine-Ore Reduction, a PRIMETALS process (Japan), with a pilot line in Austria

iBLUE: H2-DR based on ENERGIRON and EAF with CCUS of GHG emissions

IEA: Intenational Energy Agency, Paris

JFE: JFE Steel, JFEスチール, Japan

LKAB: Luossavaara-Kiirunavaara AB, Sweden

MIDREX: company and process name, stemmed formerly from Midland-Ross Direct Reduction, USA

NG: Natural Gas

OPEX: Operating Cost

OSBF: Open Slag Bath Furnace

PEM: Proton Exchange Membrane

PEME: PEM electrolyzer

PRIMETALS: PRIMETALS Technologies a joint venture of Siemens, Mitsubishi Heavy Industries, now fully owned by MHI

REN: Renewable Energy

SAF: Submerged Arc Furnace

SALCOS: Salzgitter Low CO2 Steelmaking, Germany

SHS: Stahl-Holding-Saar GmbH, Germany

SOEC: Solid Oxide Electrolysis Cell

SOFC: Solid Oxide Fuel Cell

SSH: Social Sciences & Humanities

SSAB: Svenskt Stål AB, Sweden

STEM: Science Technology Engineering Mathematics

SUPER-COURSE50: Japanese program following up on COURSE50

SuSTEEL: Sustainable Steel Program, Austria

TKS: ThyssenKrupp Steel, Germany

TRL: Technology Readiness Level

ULCOS: ULtra LOw CO2 Steelmaking, an EU research program

USS: US Steel Corporation

WHO: World Health Organization

References

- B. Latour, Où atterrir, comment s’orienter en politique, La Découverte, 2017, 156 p. [Google Scholar]

- CO2-Earth, Global Carbon Project, https://www.co2.earth/global-co2-emissions [Google Scholar]

- M. Crippa, D. Guizzardi, M. Banja, et al., CO2 emissions of all world countries, in: JRC Science for Policy Report, European Commission, EUR 31182 EN, 2022 [Google Scholar]

- P.R. Shukla, R. Slade, A. Al Khourdajie, et al., Climate Change 2022, Mitigation of Climate Change Summary for Policymakers, Working Group III contribution to the WGIII Sixth Assessment Report of the Intergovernmental Panel on Climate Change, IPCC, 2022, ISBN 978-92-9169-160-9 [Google Scholar]

- Land Use, Land-Use Change and Forestry (LULUCF), United Nations, Climate Change, https://unfccc.int/topics/land-use/workstreams/land-use-land-use-change-and-forestry-lulucf [Google Scholar]

- EU Carbon Price Tracker, The latest data on EU ETS carbon prices, https://ember-climate.org/data/data-tools/carbon-price-viewer/ [Google Scholar]

- I. Matino, V. Colla (Eds.), Overview, state of the art, recent developments and future trends regarding hydrogen route for a green steel making process, Mater. Tech 110(2) (2022), special issue, https://www.mattech-jo2022urnal.org/component/toc/?task=topic&id=1591 [Google Scholar]

- F. Patisson, O. Mirgaux, J.-P. Birat, Hydrogen steelmaking. Part 1: physical chemistry and process metallurgy, Mater. Tech. 109(3–4), 303 (2021) [CrossRef] [EDP Sciences] [Google Scholar]

- J.-P. Birat, F. Patisson, O. Mirgaux, Hydrogen steelmaking, part 2: competition with other zero-carbon steelmaking solutions and geopolitical issues, Mater. Tech. 109(3–4), 307 (2021) [CrossRef] [EDP Sciences] [Google Scholar]

- B. Sovacool, Industrial decarbonization via hydrogen: a critical and systematic review of develop-ments, socio-technical systems and policy options, Energy Res. Soc. Sci. 80(102208), 1–65 (2021) [Google Scholar]

- L. Ren, S. Zhou, X. Ou, The carbon reduction potential of hydrogen in the low carbon transition of the iron and steel industry: the case of China, Renew. Sustain. Energy Rev. 171, 113026 (2023) [CrossRef] [Google Scholar]

- S. Pye, D. Welsby, W. McDowall, et al., Regional uptake of direct reduction iron production using hydrogen under climate policy, Energy and Climate Change (2022) [Google Scholar]

- W. Sun, Q. Wang, Z. Zheng, et al., Material-energy-emission nexus in the integrated iron and steel industry, Energy Convers. Manag. 213, 112828 (2020) [CrossRef] [Google Scholar]

- MIDREX NG, MIDREX, https://www.midrex.com/technology/midrex-process/midrex-ng/ [Google Scholar]

- M. Corbella, Production of green pig iron without CO2 emissions, A proven CO2-free alternative to Blast Furnaces production,. Tenova S.p.A., Partnership event@EUGREENWEEK, 30 May–6 June 2022, CSP Webinar, online [Google Scholar]

- MIDREX®, The world’s leading DRI production process, https://www.primetals.com/portfolio/ironmaking/midrexr [Google Scholar]

- B.J. Macmullan, Le procédé “H-Iron”, Rev. Met. Paris 61(7–8), 635–638 (1964) [CrossRef] [EDP Sciences] [Google Scholar]

- CIRCORED hydrogen-based reduction, METSO-OTTO-TEC, https://www.mogroup.com/portfolio/circored-hydrogen-based-reduction/ [Google Scholar]

- Zero-Carbon HYFOR direct-reduction pilot plant starts operation, 2021, https://magazine.primetals.com/2021/06/24/zero-carbon-hyfor-direct-reduction-pilot-plant-commences-operation-in-donawitz-austria/ [Google Scholar]

- R. Eisl, M. Hochwimmer, C. Oppeneiger, et al., Hydrogen based direct iron ore reduction plant simulation, BHM Berg- und Hüttenmännische Monatshefte 167, 92–98 (2022), https://doi.org/10.1007/s00501-022-01199-2 [CrossRef] [Google Scholar]

- POSCO starts to design the HyREX demonstration plant, 2022/08/23, POSCO, https://newsroom.posco.com/en/posco-starts-to-design-the-hyrex-demonstration-plant/ [Google Scholar]

- O. Hessling, M. Tottie, D. Sichen, Experimental study on hydrogen reduction of industrial fines in fluidized bed, Ironmak. Steelmak. 48(8), 936–943 (2021) [CrossRef] [Google Scholar]

- https://www.energy.gov/sites/prod/files/2016/12/f34/fcto_h2atscale_workshop_sohn.pdf [Google Scholar]

- T. Wolfinger, D. Spreitzer, J. Schenk, Using iron ore ultra-fines for hydrogen-based fluidized bed direct reduction—A mathematical evaluation, Materials 15, 3943 (2022), https://doi.org/10.3390/ma15113943 [CrossRef] [Google Scholar]

- J. Murilo Mourão, I. Cameron, M. Huerta, et al., Comparison of sinter and pellet usage in an integrated steel plant, Technical contribution to the 43rd Ironmaking and Raw Materials Seminar, in: 12th Brazilian Symposium on Iron Ore and 1st Brazilian Symposium on Agglomeration of Iron Ore, September 1st to 4th, 2013, Belo Horizonte, MG, Brazil [Google Scholar]

- J.J. Poveromo, Iron ores, chapter 8, in: The making, shaping and treating of steel, 11th ed., Ironmaking volume [Google Scholar]

- C. Barrington, J.J. Poveromo, DRI and the pathway to carbon-neutral steelmaking: iron ore challenges, 2022 Sustainable industrial processing summit and exhibition Volume 1, in: International Symposium on Sustainable Iron and Steel Making [Google Scholar]

- M. Ericson, RMG Consulting, personal communication, 2022 [Google Scholar]

- P. Buchholz, M. Ericsson, V. Steinbach, Breakthrough technologies and innovations along the mineral raw materials supply chain — towards a sustainable and secure supply, Miner. Econ. 35, 345–347 (2022) [CrossRef] [Google Scholar]

- LKAB, Today’s waste becomes tomorrow’s resources, The ReeMAP Project, https://ree-map.com/about-reemap/reemap-industrial-park/ [Google Scholar]

- Open Slag Bath Furnace for Hot Metal production (OSBF), https://tenova.com/technologies/open-slag-bath-furnace-hot-metal-production-osbf [Google Scholar]

- P. Cavaliere, Hydrogen assisted direct reduction of iron oxides, Springer, 2022, 399 p. [CrossRef] [Google Scholar]

- Open Slag Bath Smelting Plant, METSO-OUTOTEC, https://www.mogroup.com/portfolio/open-slag-bath-smelting-plant/ [Google Scholar]

- P. Cavaliere, A. Perrone, A. Silvello, et al., Integration of open slag bath furnace with direct reduction reactors for new-generation steelmaking, Metals 12, 203 (2022) [CrossRef] [Google Scholar]

- F. Ahrenhold, TKS, Hydrogen Iron & Steel Making Forum 2022, Stockholm, 12–13 October, 2022 [Google Scholar]

- tkH2Steel®: with hydrogen toward carbon-neutral steel, https://www.thyssenkrupp-steel.com/en/company/sustainability/climate-strategy/ [Google Scholar]

- Neutralité carbone : objectif 2050, ArcelorMittal France, https://france.arcelormittal.com/neutralite-carbone/ [Google Scholar]

- Tata Steel, the leading international steelmaker, has announced plans to pursue a fully sustainable future for its steelworks in IJmuiden, the Netherlands, by adopting a hydrogen route, Tata Steel Europe, 15 September 2021, https://www.tatasteeleurope.com/corporate/news/tata-steel-opts-for-hydrogen-route-at-its-ijmuiden-steelworks [Google Scholar]

- D. Algermissen, New “slags” for the cement industry, Partnership event@EUGREENWEEK, 30 May–6 June 2022, CSP Webinar, online [Google Scholar]

- J.-P. Birat, J.-M. Delbecq, E. Hess, et al., Slag, steel and greenhouse gases, La revue de Métallurgie-CIT, 13–21 (2002) [CrossRef] [EDP Sciences] [Google Scholar]

- Direct Reduced Iron (DRI), IIMA, https://www.metallics.org/dri.html [Google Scholar]

- CALDERYS refractory solutions to support steelmakers towards their transition to green steel, https://www.calderys.com/news/calderys-refractory-solutions-to-support-steelmakers-towards-their-transition-to-green-steel [Google Scholar]

- KELSEN tackles the technology challenges facing refractory products for the iron and steel industry by participating in the H-ACERO project, https://www.calcinor.com/en/news/corporative/h-acero-project [Google Scholar]

- T. Leber, S. Madeo, T. Tonnesen, et al., Corrosion of bauxite-based refractory castables and matrix components in hydrogen containing atmosphere, Int. J. Ceram. Eng. Sci. 4, 16–22 (2022) [CrossRef] [Google Scholar]

- S. Li, D. Chen, H. Gu, et al., Investigation on application prospect of refractories for hydrogen metallurgy: the enlightenment from the reaction between commercial brown corundum and hydrogen. Materials 15, 7022 (2022) [CrossRef] [Google Scholar]

- J.G. Hemrick, Refractory issues related to the use of hydrogen as an alternative fuel, Am. Ceram. Soc. Bull. 101(2), www.ceramics.org [Google Scholar]

- M. Dargaud, Development of refractory solutions to ensure the sustainable transition to green hydrogen-based steelmaking, in: “H2 for Green Steel, 2nd International Conference”, Jouy-en-Josas, 29 November−1st December, 2022 [Google Scholar]

- B. Nakanishi, Ceramics for enhanced hydrogen heating: challenges and opportunities for improving combustion, energy efficiency, and material compatibility, in: “H2 for Green Steel, 2nd International Conference”, Jouy-en-Josas, 29 November−1st December, 2022 [Google Scholar]

- Electrolyzers, IEA, 2022, https://www.iea.org/reports/electrolyzers [Google Scholar]

- A. Zaccara, A. Petrucciani, I. Matino, et al., Renewable hydrogen production processes for the off-gas valorization in integrated steelworks through hydrogen intensified methane and methanol syntheses, Metals 10, 1535 (2020), https://doi.org/10.3390/met10111535 [CrossRef] [Google Scholar]

- S. Shiva Kumar, V. Himabindu, Hydrogen production by PEM water electrolysis − A review, Mater. Sci. Energy Technol. 2, 442–454 (2019) [Google Scholar]

- Siemens Energy and Air Liquid form a joint venture for the European production of large scale renewable hydrogen electrolyzers, Press release, 23 June 2022, https://press.siemens-energy.com/global/en/pressrelease/siemens-energy-and-air-liquide-form-joint-venture-european-production-large-scale [Google Scholar]

- Green hydrogen: John Cockerill takes another step towards setting up a gigafactory in France, Press release, 12 June 2021, https://johncockerill.com/en/press-and-news/news/green-hydrogen-john-cockerill-takes-another-step-towards-setting-up-a-gigafactory-in-france/ [Google Scholar]

- John Cockerill to develop mega electrolyzer factory in Morocco, Process Worldwide, 12 January 2023, https://www.process-worldwide.com/john-cockerill-to-develop-mega-electrolyzer-factory-in-morocco-a-6329f565719d7290f873732c017c45c9/ [Google Scholar]

- World’s largest high-temperature electrolyzer achieves record efficiency, Salzgitter Press Release, 19 April 2022, https://www.salzgitter-ag.com/en/newsroom/press-releases/details/worlds-largest-high-temperature-electrolyzer-achieves-record-efficiency-19500.html [Google Scholar]

- S. Bouckaert, A. Fernandez Pales, C. McGlade, et al., Laszlo Varro, Davide D’Ambrosio and Thomas Spencer (core team), Net Zero by 2050 – A roadmap for the global energy sector, IEA, 2021, https://iea.blob.core.windows.net/assets/deebef5d-0c34-4539-9d0c-10b13d840027/NetZeroby2050-ARoadmapfortheGlobalEnergySector_CORR.pdf [Google Scholar]

- S. Cornot, La sidérurgie européenne se prépare pour être à la pointe de la décarbonation, Notes de l’IFRI, 2023 [Google Scholar]

- J.-P. Birat, A. Carvallo Aceves, Territorial sustainability footprint, Rev. Métall. 109, 323–331 (2012) [CrossRef] [EDP Sciences] [Google Scholar]

- D. Gielen, D. Saygin, E. Taibi, et al., Renewables-based decarbonization and relocation of iron and steel making: a case study. J. Ind. Ecol. 1–13 (2020) [Google Scholar]

- A faster pace and higher targets in LKAB’s transition towards a sustainable future, 26 April 2022, https://lkab.com/en/press/a-faster-pace-and-higher-targets-in-lkabs-transition-towards-a-sustainable-future/ [Google Scholar]

- Fit for 55, European Commission, 11 November 2022, https://www.consilium.europa.eu/en/policies/green-deal/fit-for-55-the-eu-plan-for-a-green-transition/ [Google Scholar]

- J. Wilkins, K. Kinetic, S. Kinetic, et al., Steam bio-oil reformation for carbon negative steel production at Charm Industrial, in: SAM-16 conference, 8–9 November 2022, online [Google Scholar]

- E. Bellevrat, P. Menanteau, Introducing carbon constraint in the steel sector: ULCOS scenarios and economic modeling, La Revue de Métallurgie-CIT, 318–324 (2009) [CrossRef] [EDP Sciences] [Google Scholar]

- JP. Birat, JP. Lorrain, Y. de Lassat, The “CO2 tool”: CO2 emissions and energy consumption of existing and breakthrough steelmaking routes, La Revue de Métallurgie-CIT, 325–333 (2009) [CrossRef] [EDP Sciences] [Google Scholar]

- JP. Birat, JP. Lorrain, Y. de Lassat, The “cost tool”, La Revue de Métallurgie-CIT, 337–349 (2009) [CrossRef] [EDP Sciences] [Google Scholar]

- S. Budinis, P. Levi, H. Mandová, et al., Iron and steel technology roadmap, towards more sustainable steelmaking, 2020, https://iea.blob.core.windows.net/assets/eb0c8ec1-3665-4959-97d0-187ceca189a8/Iron_and_Steel_Technology_Roadmap.pdf [Google Scholar]

- Making Net-Zero Steel Possible, An industry-backed, 1.5 °C-aligned transition strategy, Steel transition strategy, 2022, 80 p. [Google Scholar]

- C. Bataille, S. Stiebert, F.G.N. Li, Net Zero Steel, Global Facility Level Net-Zero Steel Pathways, Technical Report on the First Scenarios of The Net-Zero Steel Project, IDDRI-Global energy monitor, 2021, 32 p [Google Scholar]

- P. Chaubal, Decarbonizing steel production: challenges & opportunities, in: 4th EMECR – International Conference on Energy and Material Efficiency and CO2 Reduction in the Steel Industry 2022, 7 June 2022 [Google Scholar]

- Climate Action Report 2 July 2021, ArcelorMittal, 68 p., https://constructalia.arcelormittal.com/files/Climate_Action_Report_2_July_2021-94aa5d83ef86cd03ec059ef8d1728966.pdf [Google Scholar]

- What we do, Northern Lights, 2022, https://norlights.com/what-we-do/ [Google Scholar]

- Tenova to supply DRI technology for ArcelorMittal Dofasco plant in Canada, 14 October 2022, https://greensteelworld.com/tenova-to-supply-dri-technology-for-arcelormittal-dofasco-plant-in-canada [Google Scholar]

- https://greensteelworld.com/tata-steel-selects-mcdermott-to-manage-hydrogen-based-steel-production [Google Scholar]

- https://salcos.salzgitter-ag.com/en/index.html [Google Scholar]

- Green Industrial Hydrogen via steam electrolysis, H 2020 project, https://cordis.europa.eu/project/id/826350 [Google Scholar]

- https://www.stahl-holding-saar.de/shs/en/holding/sustainability/sustainable-steel-production/index.shtml [Google Scholar]

- Our path to a green future, voestalpîne, https://www.voestalpine.com/blog/en/commitment/greentec-steel/our-path-to-a-green-future/ [Google Scholar]

- H2FUTURE: world’s largest “green” hydrogen pilot facility successfully commences operation, voestalpine, https://www.voestalpine.com/group/en/media/press-releases/2019-11-11-h2future-worlds-largest-green-hydrogen-pilot-facility-successfully-commences-operation/ [Google Scholar]

- M. Pei, M. Petäjäniemi, A. Regnell, et al., Toward a fossil free future with HYBRIT: development of iron and steelmaking technology in Sweden and Finland, Metals 10, 972 (2020), https://doi.org/10.3390/met10070972 [CrossRef] [Google Scholar]

- ECONIQ™: The world’s first net-zero steel, NUCOR, https://nucor.com/econiq [Google Scholar]

- Roadmap to 2050, US Steel, https://www.ussteel.com/roadmap-to-2050 [Google Scholar]

- A. Eggert, Enabling policy framework for innovative technologies as key for steel transition, The Clean Steel Partnership, “A driver to net zero, from research to deployment of ground-breaking technologies for steel”, ESTEP seminar, 1st June 2022 [Google Scholar]

- V. Vogl, F. Sanchez, T. Gerres, et al., Green Steel tracker, 2021, https://www.industrytransition.org/green-steel-tracker/ [Google Scholar]

- To the future of the low carbon blast furnace CO2 ultimate reduction system for Cool Earth 50 (COURSE50) project, https://www.course50.com/en/ [Google Scholar]

- S. Nomura, Chapter 23 – Low carbon ironmaking technologies: Japan’s approach, in iron ore (second edition), in: Mineralogy, processing and environmental Sustainability, Woodhead Publishing Series in Metals and Surface Engineering, 2022, pp. 751–776 [Google Scholar]

- K. Hase, JFE Steel, Hydrogen Iron & Steel Making Forum 2022, Stockholm, 12–13 October, 2022 [Google Scholar]

- X. Mao, Baowu, Hydrogen Iron & Steel Making Forum 2022, Stockholm, 12–13 October, 2022 [Google Scholar]

- https://www.danieli.com/en/news-media/news/second-ENERGIRON-dri-plant-china_37_743.htm# [Google Scholar]

- https://www.hbisco.com/site/en/groupnewssub/info/2021/15999.html [Google Scholar]

- W. Hall, S. Kumar, S. Kashyap, et al., Achieving green steel: roadmap to a net zero steel sector in India, The Energy and Resources institute (TERi), New Delhi, 2022 [Google Scholar]

- J.-P. Birat, La décarbonation de la filière sidérurgique : les enjeux du défi de l’« acier vert », Ann. Mines Réal. Ind. 4(2024), 77–80 (2022) [Google Scholar]

- B. D’hont, The potential of hydrogen for the chemical industry, Deloitte, 2021, https://www2.deloitte.com/content/dam/Deloitte/xe/Documents/energy-resources/me_pov-hydrogen-chemical-industry.pdf [Google Scholar]

- F.T.C. Röben, N. Schöne, U. Bau, et al., Decarbonizing copper production by power-to-hydrogen: a techno-economic analysis, J. Clean. Prod. 306, 127191 (2021) [CrossRef] [Google Scholar]

- D. Perilli, Green hydrogen for grey cement, Global Cement, 2020, https://www.globalcement.com/news/item/11061-green-hydrogen-for-grey-cement [Google Scholar]

- Technology Roadmap, Low-Carbon Transition in the Cement Industry, IEA, 2018, 61 p., https://iea.blob.core.windows.net/assets/cbaa3da1-fd61-4c2a-8719-31538f59b54f/TechnologyRoadmapLowCarbonTransitionintheCementIndustry.pdf [Google Scholar]

- Présentation de la stratégie nationale pour le développement de l’hydrogène décarboné en France, 2020, https://www.economie.gouv.fr/presentation-strategie-nationale-developpement-hydrogene-decarbone-france# et https://minefi.hosting.augure.com/Augure_Minefi/r/ContenuEnLigne/Download?id=5C30E7B2-2092-4339-8B92-FE24984E8E42&filename=DP%20-%20Stratégie%20nationale%20pour%20le%20développement%20de%20l%27hydrogène%20décarboné%20en%20France.pdf [Google Scholar]